Streaming Content Budgets in 2023: Trends and Predictions

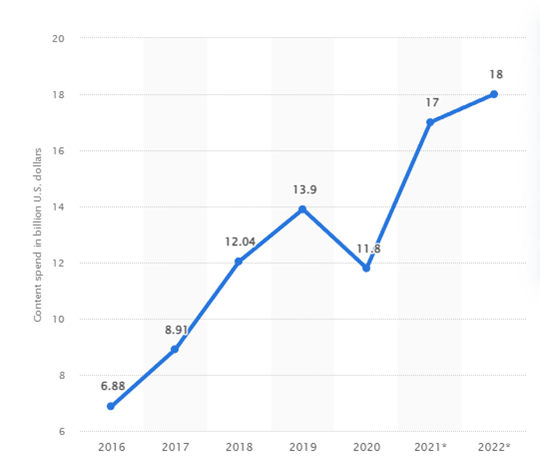

It’s been a decade of nearly nonstop growth in content investments for streaming services, networks, and studios. In 2022, the industry spent a record $238 billion on content to attract, engage, and retain audience.

And for good reason; the recent research report Optimizing Video: Enhancing Content Performance for OTT Success examines drivers of monetization on OTT streaming platforms with data from research frim Parks Associates.

Of course it’s content. More specifically, content that will compel viewers who are perfectly comfortable stacking multiple streaming services, cancelling subscriptions, and flipping to more than 3,700 FAST channel options (36% more than a year ago) with one click, swipe, or voice command.

But as recent economic pressures impact both the demand and supply side of the market, gigantic content budgets and premium pricing aren’t as strategically viable as they’ve been to date. This posts explores what’s happening with content budgets across OTT in 2023, including:

- Content investment as a competitive strategy

- Comparative budgets for the largest streaming platforms

- Trends and predictions in content spend this year

Streaming content budgets include production and licensing

We’re defining “budget” here as the total dollar amount an OTT video platform’s spends (or plans to spend) on streaming content during a given year.

Streaming content budgets generally fall into three categories:

1) Licensed Content – Content acquired through a licensing agreement between content seller and OTT service or platform. These deals, of course, give distributers the rights offer content on their platform exchange for a revenue split. Commonly that’s based on viewing hours, but some terms involved different models such as fixed-fee.

2) Original Content – Behemoths like Disney Plus, Netflix, HBO Max, and Amazon Prime Video have increasingly invested in acquiring or producing originals: Netflix’s Squid Game and Stranger Things, Amazon’s The Lord of the Rings: The Rings of Power and The Boys, and HBO’s White Lotus. Exclusivity terms for original content vary, with Disney famously favoring a closed ecosystem and HBO distributing through aggregators like Prime Video.

3) Purchased Content – OTT services may expand their content offerings by outright purchasing rights to individual video assets or libraries from rights holders or, as commonly seen in M&A, entire catalogues. (See Amazon’s 2022 acquisition of MGM Studios, which saw the streaming giant take over rights to more than 4,000 film titles and 17,000 TV episodes.)

Streaming content budgets drive growth for OTT platforms… historically

OTT video streaming services compete by optimizing multiple variables. UX, quality of service, ad placement, pricing, and other factors all impact the ability to monetize.

But there’s one factor that supersedes the rest when it comes to competing successfully in the OTT streaming marketplace: content affinity.

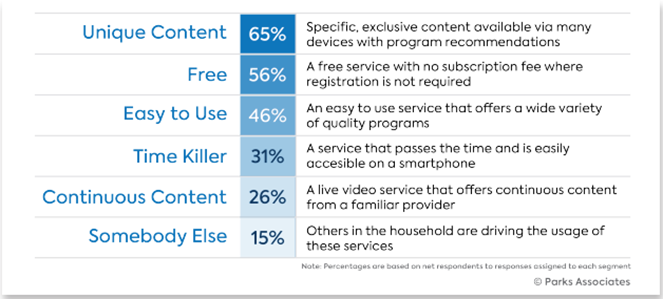

Parks Associates found that 48% of consumers say that the presence of desirable content or a specific program was their primary motivation for subscribing to a new OTT service. For ad-supported services, 65% of respondents said that unique content was their primary motivating factor when starting a subscription. A bevy of OTT statistics prove that content spend is a weighty decision for streaming platforms.

Which OTT platforms have the largest streaming content budgets?

Subscription-based video on demand (SVOD) platforms has been the industry’s cash cow for years, with the largest streaming content budgets of all OTT services.

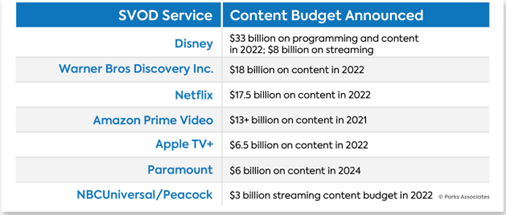

Disney historically leads the way, with an announced annual spend of $33 billion in 2022 (an $8 billion increase from the previous year). That includes original content for its major franchises (e.g. Star Wars, Marvel, Pixar Universe, etc.), but also its licensed content (notably, live sports). Disney is also projected to have the highest growth in content investment of any streaming service in 2023, compared to relatively restrained growth in competitors’ spend.

The mass media conglomerate Warner Bros Discovery Inc., the product of Warner Bros. and Discovery’s 2022 merger, is fast-tracking the release of its new OTT streaming service. With a target of 130 million global DTC subscribers by 2025, the company plans to attract new users by spending $9.5 billion on content in 2023.

Netflix had a streaming content budget of just $1 billion in 2010, but increased competition from a growing number of OTT service providers has led the OTT pioneer to grow its content spending every year since. Accordingly, Netflix spent $17.5 billion on content in 2022.

Amazon Prime Video is another big spender on content, with a reported streaming budget of $15 billion in 2022. There’s also Apple TV+, which spent $6.5 billion on content in last year, and NBCUniversal, who spent $3 billion on content for its direct-to-consumer streaming platforms in 2022.

How will streaming content budgets change in 2023?

In the short history of OTT video streaming, platforms have relied on steadily increasing investments in content acquisition to drive subscriber and revenue growth – but that appears to be changing in 2023.

The OTT streaming market is reaching maturity and services are no longer achieving the high rates of subscriber growth that were common over the past decade. The rate of cord-cutting outpaces itself daily, but growing competition from emerging FAST and AVOD services means that the SVOD model isn’t winning as many of those customers. Economic concerns over inflation and fears of a recession are also pushing audiences away from paid streaming services.

These factors have changed the growth outlook for major streaming services, resulting in a financially challenging year for the OTT industry’s largest content spenders in 2022. Disney, Warner Bros. Discovery, NBCUniversal, and Paramount streaming services all lost money. Disney missed earnings targets and saw its share price drop by over 30%, while Netflix’s share price fell by 35% over the past year, and Warner Bros. Discovery shares fell 48.5% during the same period. And all of this happened while the three firms spent a combined total of almost $70 billion on content.

Warner Bros. Discovery CEO David Zaslav was quoted saying that “The strategy to collapse all windows, starve linear and theatrical and spend money with abandon, while making a fraction in return, all in the service of growing sub numbers, has ultimately proven, in our view, to be deeply flawed.”

Based on these factors, it’s more than likely that the era of consistent, large increases in OTT content spending is coming to an end. In an environment where subscriber growth is slowing down, we expect OTT platforms to slow down the growth in their content spending and explore new strategies and business models to drive profitability.

Large streaming content budgets means opportunity for content sellers

Despite concerns about the long-term growth outlook for SVOD streaming platforms, there’s no indication that OTT content budgets will necessarily be declining in the near future. But content spending is predicted to level off or, at best, continue at a more modest growth rate. Today’s big players in content spending will still need plenty of fresh and exciting content to drive subscriber engagement and mitigate churn.

In a January 2023 report, Ampere Analysis predicted that global content expenditure would increase by just 2% annually, compared to 6% in 2022. Linear budgets will continue to be trimmed at a steady clip while Disney, Apple, and Netflix will budgets are expected to see a relatively larger increase than OTT competitors.

Economic headwinds across the globe will put pressure on household spending and advertising investment, leading to companies implementing cost-saving measures and reducing content expenditure. -Ampere Analysis

More content insights

Ready to learn more? See additional research insights and analysis in Optimizing Video: Enhancing Content Performance for OTT Success.

In addition to highlighting the latest trends in OTT streaming content budgets for 2023, this white paper explores the role of content in driving cost and benefit for OTT platforms, the impact of growing business models like FAST and AVOD, the emergence of evolved content partnership structures in the OTT industry, and the best new opportunities for content sellers to maximize licensing revenue with data analytics technology.