The FAST Slow-Down: Four Factors Behind FAST’s Sluggish Revenue

Viewership on Free Ad-supported Streaming TV (FAST) platforms like Pluto TV and Tubi is continuing to rise, but slow revenue growth and low revenue-per-user on FAST services are leaving content sellers unsure about whether to move their content to FAST.

Rather than going all-in on FAST distribution, content sellers are currently driving viewers to subscription-based platforms by teasing high-value content on FAST or distributing certain high-value media assets exclusively on Pay TV to protect MVPD relationships.

FAST service providers have a massive opportunity to compete with traditional MVPDs through an alternative lean-back viewing experience, but major broadcasters and cable-satellite content creators simply won’t transition their content onto FAST platforms until it’s economically viable to do so – which means that FAST platforms need to start making more money.

In this blog, we’re taking a closer look at the state of FAST revenue: how much revenue is being generated by FAST services, four factors behind the industry’s sluggish revenue performance, and how FAST service providers can take action to accelerate revenue growth.

The state of FAST revenue in 2023

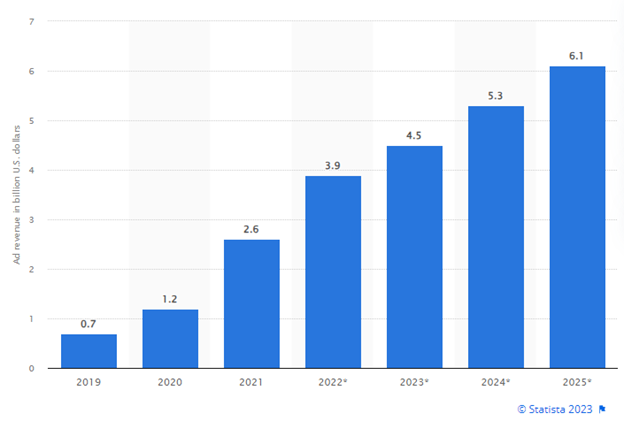

FAST platforms in the U.S. are projected to generate approximately $4.5 billion in revenue in 2023, up from $2.6 billion in 2021 and around $3.9 billion in 2022. The majority of that revenue is split between 22 major FAST streaming services (e.g. Pluto TV, Tubi, the Roku Channel, Samsung TV Plus, etc.) and numerous content sellers who distribute their TV and video media assets across more than 1,400 FAST channels.

Leading FAST service providers have seen substantial growth in viewership over the past several years. The Roku Channel grew from 30 million monthly active users in early 2019 to more than 71 million in 2023, Tubi grew from 20 million to 64 million monthly active users in the same time period, and Pluto TV has grown from ~30 million monthly active users in 2020 to more than 80 million today.

Comparing FAST revenue with alternative distribution models

Average Revenue per User (ARPU) is a metric used by media distribution companies to measure how effectively a distribution platform or business model is monetizing its audience.

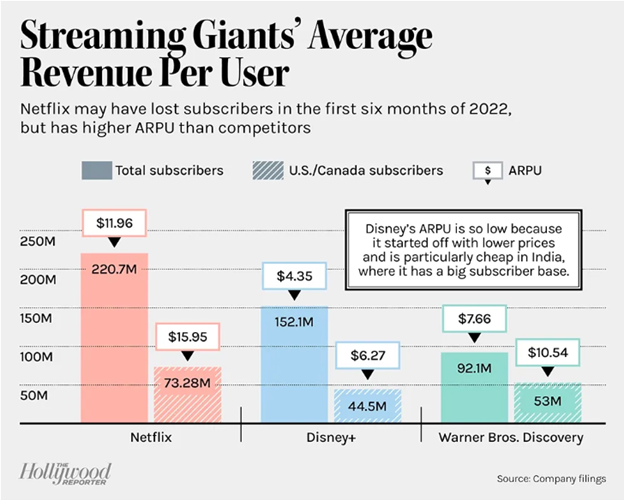

Traditional Pay TV providers have the highest ARPU, with subscribers paying an average of $107 per month or $1,284 annually for cable or satellite TV services. Then we have SVOD distributors, led by platforms like Netflix (ARPU of $16.23/month), Paramount Plus (ARPU of around $9), and Warner Media’s Max (ARPU of $11.15/month), with an overall average ARPU of $75 annually or $6.25/month.

Many FAST platforms don’t publish their ARPU numbers yet, so it’s difficult to calculate ARPU for the whole industry – however, we can look at reporting from individual FAST services to see how effectively those platforms are monetizing their audiences.

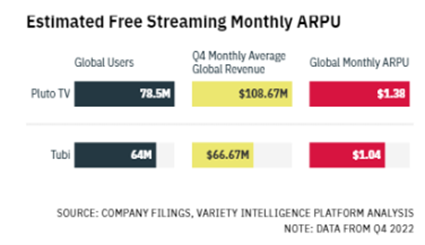

In Q4 of 2022, Pluto TV reported 78.5 global users and revenues of $108.67 million, yielding a global monthly ARPU of $1.38. Tubi is projecting $1 billion in revenues for this year based on 64 million active monthly users, for a projected ARPU of $15.63 annually or just $1.30 per month.

FAST revenue is growing, but not fast enough…

FAST is a newer distribution model than SVOD or traditional Pay TV, and FAST platforms make far less money than SVOD or Pay TV.

Tubi has roughly the same number of monthly active users as there are Pay TV subscribers in the United States (around 64 million), but generates just $1.30 per user each month compared to the $100+ per user generated by MVPDs.

To explain why FAST ARPU is not increasing as quickly as viewership, let’s look at four factors that are negatively impacting FAST revenue generation – and how platforms can address them to increase revenue and appeal to the best content sellers.

Read: 5 Ways Revedia Digital Accelerates FAST Distribution Workflows to discover how content sellers can accelerate FAST distribution workflows and reveal insights into FAST performance.

Four factors behind FAST’s slow revenue growth

1) Lack of distributor consolidation

FAST is a relatively new business model, but we’ve seen a huge influx of new FAST platforms and service providers springing up over the past few years.

With 20+ streaming platforms and over 1,400 FAST channels available, audiences have an abundance of choice. But for content sellers, the crowded market means diluted revenue opportunities while having to negotiate and manage numerous licensing agreements. There’s also a danger that content sellers can dilute the value of their content by distributing it across too many different platforms – both OTT and traditional.

FAST platform consolidation will concentrate more viewers on the top FAST platforms, generating more revenue for content sellers with less licensing agreement management overhead.

2) Lack of data sharing between FAST platforms and content sellers

FAST platforms have access to content performance and audience engagement data but don’t always share this vital information with the content sellers who create and license their video assets.

With increased data sharing and transparency from FAST distribution partners, content sellers can adjust their production and distribution strategies to deliver content that audiences want, driving increased platform engagement, ad impressions, and revenue.

3) Lack of advertising inventory and brand trust

FAST platforms that depend on advertising to generate revenue need a continuous supply of advertising inventory.

That requires building and expanding relationships with traditional Pay TV advertisers, including beverage companies, telecom and insurance providers, car manufacturers, and pharmaceutical companies.

A challenge for FAST service providers has been delivering transparency regarding how ad inventory is deployed and when/where ads are shown. In traditional linear media, advertisers have been able to purchase ad spots at a specific time of day or during a specific program. These features enable a brand-safe environment with certainty for advertisers.

But most FAST platforms haven’t provided that level of certainty. In fact, consumers often report seeing the same ads repetitively which can result in negative brand sentiment.

Purchasing ad space next to specific content is currently harder on OTT, but given the wealth of data that FAST platforms can gather about their users, highly targeted advertising is surely coming soon. In the meantime, advertisers may need to accept general impressions.

4) Lack of sophisticated advertising technology

FAST streaming providers need more sophisticated advertising technology to improve ad placements and deliver a more targeted/personalized advertising experience for audiences. Just like other platforms that charge more for highly targeted ad placements, FAST platforms can increase their advertising CPM by effectively targeting ad placements at the most qualified users.

With better advertising tech, FAST platforms can start leveraging their internal data to deliver more targeted ad placements. For example, a FAST platform could identify users by their IP address, track each user’s engagement history to understand their content preferences or interests, then use that information to deliver more targeted ads.

As ad targeting improves, FAST channels can deliver better results for advertisers and increase revenue by charging a higher CPM for more targeted ad placements.

The road to revenue growth for FAST service providers

FAST service providers have four main ways to increase revenue:

- Expanding viewership via user acquisition or platform consolidation.

- Driving audience engagement so viewers watch for longer and consume more ads.

- Running more advertisements per hour viewed requires sufficient ad inventory and risks upsetting viewers.

- Charging more for ad placements ideally through improved targeting/personalization.

As market leaders like Samsung TV Plus, Pluto TV, and the Roku Channel continue to capture the lion’s share of FAST viewership growth, we’re expecting movement towards distributor consolidation that can simplify licensing management for content sellers. Hardware could be an important driver here, as CTV manufacturers like Samsung, LG, and Roku leverage their dominance in the Smart TV market to extend the reach of their FAST services.

Until then, FAST platforms should focus on building advertiser relationships, improving ad targeting/personalization capabilities, and sharing data with content sellers to drive engagement and revenue growth.

If their efforts are successful, FAST platforms will attract the big-spending advertisers and high-value content they need to build services that can compete with MVPDs in the media distribution market.

Monetize your content on FAST services with Revedia Digital

Licensing management workflows have become increasingly complex and time-consuming for content sellers distributing their assets on FAST platforms.

Revedia Digital is a data intelligence platform that helps content sellers streamline and automate licensing management workflows, track distributor performance, and efficiently manage and forecast revenue.

Ready to learn more?

Check out our free white paper Monetizing Content via Free Ad-Supported Streaming TV to get the latest insights into the FAST video market segment and discover how Revedia Digital is helping content sellers optimize FAST distribution.