The content industry continues to be an ever-changing landscape, with one innovation (or disruption) after another shaking up the market before it can land on a new status quo. After a year that saw subscriber stagnation, the first joint strike between SAG-AFTRA and the WGA for more than sixty years, and a change of studio focus, it’s time to examine the 2024 trends affecting the media industry in Europe, Middle East, and Africa (EMEA).

While the strikes are now in the rear-view mirror, brand new content will take some time to hit theatres and TV screens again. The distribution landscape will undoubtedly feel some effect from this, but that is just one of the many trends to expect in 2024.

Studios will find new ways to monetize their content

At the start of 2023, investor pressure pushed studios to seek higher profits, with early metrics like subscriber growth not being enough to satisfy anymore. As a result, all studios have had to rethink their direct-to-consumer (D2C) strategy, manifesting change in multiple ways.

Ad-supported tiers and price hikes became more common in 2023; Netflix began clamping down on household sharing, with Disney soon following suit. On the content side, many are rethinking their approach to international distribution, with cracks starting to appear in the all-in approach that Disney and many others once adopted for vertical integration.

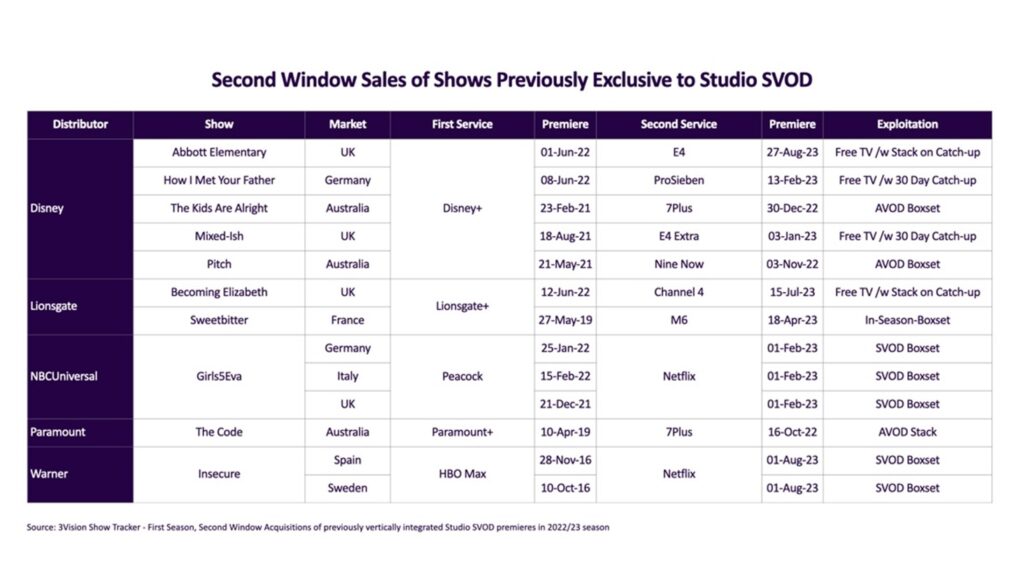

Studios are already beginning to alter their windowing strategy, licensing their library content to third-party services once again. But even at the earlier second-window stage, certain titles have a second life after debuting on their studio’s SVOD service.

Some of the early second-window activities after studio SVOD are self-explanatory. Low-profile titles, canceled after one season, like ‘The Kids are Alright’ and ‘Pitch,’ have been sold for presumably reasonable rates to free TV services in Australia. However, high-profile, ongoing series are being sold, too, such as the Emmy award-winning ‘Abbot Elementary,’ which has seen a second window on E4 in the UK while still being available to stream on Disney+. Barring unforeseen disruptions, the trend will likely continue upward in the coming year.

Second windows of digital originals on TV will close

Amazon MGM has announced its intention to distribute second windows of Amazon originals. Following a global SVOD like Netflix or Amazon is not without its drawbacks, particularly for broadcasters hoping for an acquisition to have a decent digital footprint after its linear transmission.

While second windows of true originals from Netflix and Amazon have been rare, series acquired by these services for worldwide rights (excluding the US) have seen subsequent second windows. These acquisitions were often originally branded as originals by their SVOD buyers, with broadcasters most likely to take them on in the second window.

Any level of enhanced catch-up is extremely rare in these situations, with most second windows by broadcasters having a very limited life online after transmission. This can add to a lot of frustration for buyers, who may determine that acquiring older seasons merely drives their audience to the SVOD services that offer subsequent seasons.

To succeed with these now wary buyers, Amazon MGM must be willing to grant more substantial catch-up rights, which are now a norm in most markets for both pay and free TV. If Amazon were willing to relent on the standardized second window catch-up strategy, it would put them well ahead of other SVOD services also looking to sell their content in a second window.

Unless major streaming platforms are willing to extend catch-up rights to buyers of their original series, the content’s second-window availability will likely remain limited in 2024 for EMEA media companies.

Licensing will become a buyer’s market

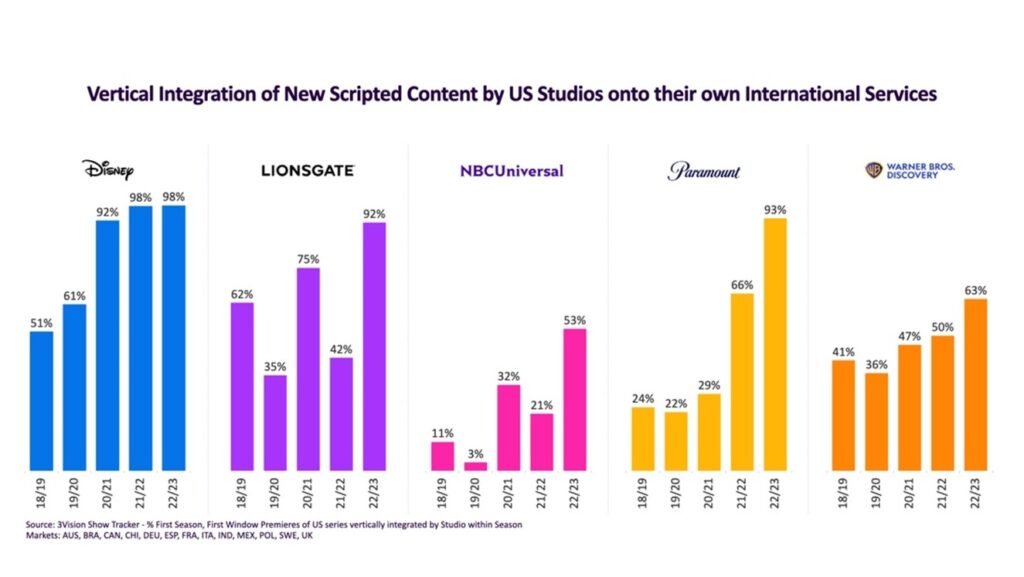

In recent years, many studios have favored vertically integrating their content onto their own SVOD services in the first window to support D2C growth. Effectively taking so much content off the market has made it especially difficult for local players to acquire content for their services.

Studios and distributors without their own D2C service were able to put high prices on their content in 2023, with the latest content only being sold to big-budget buyers like Pay TV operators and, in some cases, studio SVOD services. As studios seek new ways to monetize their content to help bring profits back up, local buyers will find themselves in a much stronger position.

Market exits for SVOD, such as Lionsgate+ across EMEA and Latin America, opened a flood of initial second-window opportunities as Starz originals went up for grabs. MGM+ acquired many of these rights in markets like Germany and Italy. This also means that Lionsgate and Starz will be pushing all their content output to third parties across these former Lionsgate+ markets.

Many broadcasters will likely be met with a flurry of offers to acquire series in a second window. But again, without significant rights granted for the highest-profile shows, they will have little interest in the second windows on offer. Studios increasingly keen to make money in this pivotal space may find themselves offering buyers more first-window opportunities to foster these relationships and encourage more acquisitions for second-window and library titles.

Looking back to look ahead

Studios may have once felt they were approaching a position where they could leave their old buyers behind, enjoying instead a global direct-to-consumer model. However, investors have forced an earlier change in strategy in EMEA media— one that will instead welcome a balanced approach between services and potential revenue. The tension now lies between the teams running SVOD services and their distribution arms, as priorities in one area will inevitably affect the other.