10 OTT Video Trends You’ll See in 2023

A lot has happened since we published our article on OTT Video Streaming Trends to Watch in 2022.

The Over-The-Top (OTT) video streaming market is continuing its growth in North America and around the world. Top video streaming providers in the OTT industry, especially in the SVOD (Subscription Video On Demand) market segment, are continuing to invest in original content and experiment with hybrid monetization strategies. At the same time, new market entrants leverage linear format models like FAST and vMVPD to target niche audiences with unique content offerings.

We’re also seeing a continued decline of around 5 million subscribers annually in Pay TV, an ongoing trend that’s pushing sports brands onto OTT platforms and driving OTT platform investments and acquisitions from Pay TV providers trying to retain a larger share of the media and entertainment market.

To break down these trends and offer additional insights into the changing landscape of the OTT market, we’ve compiled an updated list of OTT Video Trends for 2023. Keep reading to explore 10 emerging OTT trends that will shape the video streaming market in 2023 and beyond.

For additional insights, download the research paper we co-produced with Parks Associates: Optimizing Video: Enhancing Content Performance for OTT Success.

1) SVOD is Reaching Peak Maturity

The SVOD market segment has grown consistently since Netflix and Hulu launched their OTT streaming platforms in 2006. However, we’re beginning to see indicators that SVOD growth is slowing down as the market reaches maturity in the United States:

- Netflix Lost Subscribers for the first time in a decade, with a 200,000 net subscriber loss in Q1 2022 and another million net subscribers leaving in Q2.

- High Subscriber Churn Rates in SVOD (as much as 44%) have been reported across all services.

- Hybrid Revenue Models are becoming increasingly important for SVOD service providers, with Hulu generating more than $3 billion from OTT advertising and Netflix and Disney launching their own ad-supported tiers.

- SVOD Market Penetration is High, with 78% of US households having access to at least one of the top SVOD services.

As the SVOD market segment continues to mature, top SVOD video platforms (Netflix, Disney, Amazon Prime Video, HBO, etc.) are investing in content and experimenting with hybrid monetization strategies to win audiences, drive revenue, and fend off competitors – including other SVODs, as well as emerging FAST and vMVPD platforms. We expect this OTT trend to continue into 2023.

2) FAST Continues Meteoric Growth

FAST (Free Ad-supported Streaming TV) platforms have captured a growing share of the OTT market since the 2020 pandemic, and their growth isn’t slowing down.

The FAST market segment has proliferated from just a handful of fledgling services and around 700 channels in 2020 to more than 30+ FAST services and 1400 FAST channels available today. Pay TV providers have expanded their presence in the OTT streaming market (and counterbalanced declining subscriber counts) by investing in FAST platforms: Comcast owns Peacock and Xumo, Fox owns Tubi, and CBS owns Pluto TV.

Data from Q2 2022 shows that FAST subscriber engagement is rising, with 55% of US consumers regularly streaming content from at least one FAST service. That’s an increase of 9%, or nearly 30 million people compared to just six months prior. Revenue in the market segment has also grown exponentially, from around $1 billion in 2020 to an estimated $4 billion in 2022. We’re expecting more channel and platform proliferation in the FAST market segment in 2023, along with continued growth in market penetration and revenue.

3) Smart TVs Gaining in Streaming Device Market

Smart TVs are increasing market penetration in 2022 and are poised to surpass add-on streaming devices like Roku and Amazon Fire Stick as the most popular way to stream OTT video. Between February 2021 and 2022, the number of households watching OTT content on Smart TVs increased by 17% while household penetration of add-on streaming devices increased by just 5%.

Smart TVs are becoming more affordable with each passing year, and manufacturers like Samsung and LG are working to differentiate themselves with improved viewing experiences, better functionality, pre-installed streaming services, and proprietary FAST services like Samsung TV Plus and LG Channels+.

We’re also hearing more about “Subsidized TV” and the idea of Smart TV manufacturers selling TVs at cost to pull audiences into their ecosystem and monetize them – either through targeted advertisements or by selling their data to third parties. We expect household penetration and overall viewership of Smart TVs to keep increasing through 2023, displacing viewership on add-on streaming devices, laptops, and mobile devices.

4) OTT Distributor Consolidation Continues

Mergers and acquisitions have always shaped and reshaped the media and entertainment landscape, but we’re seeing a recent OTT trend that acquisitions could be on the rise. M&A activity in the media and telecom industries for the 12 months ending on May 15th included 1,014 deals (up 28% from the previous 12-month period) valued at $469 billion.

Amazon’s $8.45 billion takeover of MGM and AT&T’s $43 billion sale of WarnerMedia to Discovery both closed this past year, and there’s plenty of speculation about what could be coming next. Lionsgate is poised to sell a stake in Starz to the right buyer, while cash-flush YouTube and Apple TV might be looking at acquiring production studios to pump out original content for their OTT streaming services.

We’re seeing high levels of OTT distributor consolidation as established media companies seek to acquire up-and-coming video streaming services with innovative capabilities and established audiences. One example is Comcast, who purchased the FAST platform Xumo while already owning Peacock. Another is CBS, who purchased Pluto TV through its Paramount Streaming subsidiary while already owning Paramount+. These companies will likely use their newly-acquired FAST services as lead-generation tools for paid services.

We’re expecting the trend of OTT distribution consolidation to continue through 2023 and beyond, especially if we continue to see a high volume of M&A activity.

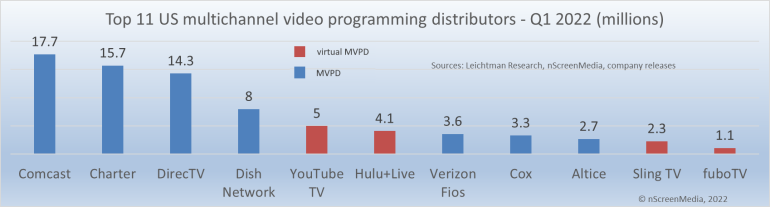

5) vMVPDs Will Win More Subscribers

As the cord-cutting trend continues and Pay TV subscriber counts continue to decline, vMVPDs (virtual Multichannel Video Programming Distributors) like Fubo, YouTube TV, and Sling TV are attracting wider audiences.

These vMVPDs present live television content in a linear format to audiences over the Internet, with each service provider offering a package of channels similar to a cable TV line-up, but at a lower cost than a monthly Pay TV subscription. These trimmed-down virtual cable packages give audiences the variety of content they’re used to, but without the high subscription costs associated with traditional Pay TV.

The total number of vMVPD subscriptions in the United States reached 14 million in Q3 2021, and is expected to grow to 23 million by 2024. We expect to see vMVPDs keep gaining momentum by pulling subscribers away from Pay TV and SVOD.

6) Sports Brands Continue Expansion into OTT Streaming

Live sports have acted as a buoyant force for traditional Pay TV providers during the last two decades of declining subscriber counts, but we’re increasingly seeing the world’s leading sports brands expanding into OTT distribution, especially through vMVPDs and Direct-to-Consumer (DTC) streaming platforms.

vMVPDs like Fubo TV are offering European soccer channels, the MLB Network, and niche sports channels like Impact Wrestling and Fox Sports Racing. Audiences can now watch NFL games without a cable subscription using services like YouTube TV, Sling TV, the Fox Sports app, Paramount Plus, and Hulu + Live TV. Live streaming NBA games appear on multiple services, including AT&T Live, Hulu + Live TV, and Disney’s ESPN.

On the DTC side, we’re seeing sports brands launch proprietary subscription-based streaming apps where super-fans can subscribe to watch live games and access exclusive content. Examples include the NFL+ mobile app, NBA League Pass, and F1TV.

As we move into 2023, we expect to see a growing number of sports brands expand their OTT content distribution to reach a wider audience and drive revenue.

7) Diverging Distribution Models Stratify OTT Video Content

In just the past three years, we’ve seen the OTT video streaming market start to diversify with new and emerging distribution models – especially FAST, vMVPD, and Premium Video on Demand (PVOD).

We’re now seeing an OTT trend where video content is becoming stratified between streaming services, with high-budget content moving towards established PVOD and SVOD platforms with strong average revenue per user (ARPU). Meanwhile, low-budget, niche, nostalgic, and crowd-sourced content from independent content creators are gravitating toward FAST and AVOD (Ad-supported Video-On-Demand) services.

We’re expecting this content stratification trend to continue into 2023, especially as OTT distributor consolidation continues and large media conglomerates start using FAST services to funnel audiences toward subscription-based services with more desirable content.

8) Content Sellers Use New Software Tools to Maximize Licensing Revenue

As the OTT video streaming market grows with new platforms and innovative distribution models, it’s becoming increasingly challenging for content owners and aggregators to manage content licensing workflows across so many new OTT distributor partners to effectively monetize their content.

To make the most of their video assets, content sellers are starting to leverage AI-driven software solutions like Revedia Digital. These platforms empower content sellers to:

- Automate the process of tracking, verifying, collecting, and forecasting OTT video streaming revenue,

- Aggregate and normalize content performance, distributor performance, and financial data from multiple OTT platforms in a single source of truth,

- Manage licensing agreements, including negotiations, and renewals, and

- Calculate and process accurate royalty and revenue share payments.

As we move into 2023, we expect to see a growing number of content sellers using sophisticated software to manage, analyze, and monetize digital distributor data.

9) The Rise of OTT Video Streaming Super-Aggregators

Another OTT trend we’re excited about is the rise of OTT video streaming super-aggregators.

Amazon Prime Channels is a great example, with the new service allowing Amazon Prime Video members to subscribe to premium and specialty video streaming channels (e.g. Paramount+, AMC+, STACK TV, BritBox, Hollywood Suite, Shudder, the Smithsonian Channel, PBS Masterpiece, etc.) on a short-term basis – with low subscription fees, no long-term commitment, and no apps to download.

Following Amazon’s lead, YouTube just launched a new service called Primetime Channels that will allow audiences to access content from 34 different streaming services on the YouTube platform.

As we move into 2023, we expect to see more platforms like Amazon Prime and YouTube aggregating content from multiple streaming services in hopes of positioning themselves as the #1 destination for streaming OTT video content.

10) OTT Platforms Localizing Video Content by Geography

The final OTT trend on our list deals with OTT platforms localizing video content to meet the needs of audiences in diverse geographical settings. We’re beginning to see more localized video content in the FAST market segment, where platforms can serve local news and weather to audiences depending on their location.

Large SVOD platforms like Amazon and Netflix have already been active in developing local content for audiences in China, Japan, and India – but with global SVOD market penetration measured at around 15% and expected to increase over the next several years (especially in the EMEA market), we expect to see OTT platforms with global reach investing more heavily in localized content for niche geographical and cultural audiences around the world.

Manage OTT Streaming Revenue in 2023 with SymphonyAI Media

SymphonyAI Media is empowering content sellers and OTT distributors with AI-driven software solutions to manage and maximize streaming revenue.

Our Revedia Digital platform provides data-driven insights to help customers aggregate, normalize, and segment data from multiple platforms, automate licensing management workflows, and maximize revenue generation from video content assets.