10 OTT Video Trends You’ll See in 2024

It’s been another year of exciting developments in over-the-top (OTT) video streaming. Ad-supported entertainment is bigger than ever, SVODs are prioritizing profits over growth, MVPDs are innovating to fight for market share and relevance, and AI is playing an ever-increasing role throughout the media industry. To highlight essential events from the past year and predict where the industry is headed, we’ve compiled an updated list of the ten most important OTT video trends shaping the media industry over the next 12 months.

1) More ad-supported streaming than ever before

Free ad-supported streaming (FAST and AVOD) was the fastest-growing segment of the OTT market in 2023. As SVOD subscription fees rise and consumers continue to depart pay TV, free streaming platforms have been evolving quickly. We’ve seen FAST platforms like Pluto TV and Tubi expanding into AVOD and on-demand platforms like YouTube experimenting with linear streaming. Tubi, Roku, and Freevee were the first FAST platforms to commission original content in 2021. We expect even more investment into FAST originals in 2024 as platforms expand their audience reach and attract more advertising dollars. Meanwhile, established SVODs like Netflix, Disney+, Max, and Paramount Plus now offer ad-supported subscription tiers. Amazon Prime, one of the last major holdouts, is finally launching its ad-supported tier this month. While the proliferation of ad-supported streaming may foster market fragmentation, it should give consumers more streaming options and content sellers more ways to monetize their assets.

2) The influx of ad dollars will drive advertising innovation

Advertisers have been slow to shift their ad spend to streaming platforms thus far, for several reasons including: ● Low differentiation between free streaming providers ● Lack of capabilities for targeted advertising ● Commodification of ad inventory As a result, ad-supported streaming services have struggled to secure the inventory they need to fully maximize their revenue potential. But it’s starting to look like 2024 could be the first year streaming platforms have sufficient technology, ad sales, and unique content to fill ad spots and accelerate revenue growth. One recent report suggests that FAST ad spending will surpass cable, broadcast, and SVOD ad spending by 2025. Amazon Prime's new default ad-supported subscription tier is another catalyst for the influx of advertising dollars to free streaming platforms. The streaming giant is reportedly asking ad agencies to commit between $50-100 million in annual ad spend for 2024. We’ll also see more advertising innovation in 2024, such as Hulu’s new “Pause Ads” function and “shoppable ads” from Walmart + Peacock and Roku + Shopify.

3) Major SVODs will continue to aim for profitability over growth

Over the last 12 months, SVOD platforms hit an inflection point where U.S. subscriber growth slowed, consumers showed subscription fatigue from managing an average of 5-10 SVODs, and subscribers churned to free streaming services at record rates. Factor in shrinking content budgets due to economic headwinds, and we can see why SVODs continue to focus on consolidating their market position and prioritizing short and medium-term revenue over long-term growth. That’s why we’re seeing things like: ● SVOD market consolidation (e.g., Disney’s recent takeover of Hulu) ● SVOD subscription price increases ● Netflix and Disney cracking down on account sharing for the first time

High rates of password sharing suggest that some SVODs could grow revenue by converting password-sharing users into paying customers. (Source) As free streaming becomes more popular and SVOD becomes more exclusive, services like Netflix and Hulu that provided a low-cost alternative to traditional pay TV, are being repositioned as a premium alternative to free streaming.

4) OTT services will be bundled with telecom packages

SVOD platforms are still looking to expand customer acquisition by partnering with telecom providers who can bundle streaming services with wireless, broadband, or pay TV services. A new streaming bundle available exclusively to Verizon customers includes the ad-supported versions of both Netflix and Max for just $10/month - a savings of more than 40% off the regular price. Verizon also includes a Disney Bundle (featuring Disney Plus, Hulu, and ESPN+) with certain 5G mobile plans. T-Mobile subscribers can also benefit from free Netflix, Apple TV+, or ViX Premium (the world’s largest Spanish language streaming platform) bundled with 5G mobile phone plans. While SVOD subscriber churn is high, bundling OTT streaming with telecom services can provide more value to customers and drive acquisitions for SVODs while mitigating churn. Around 20% of SVOD subscriptions came from telecom bundles last year, and that number is expected to reach over 25% by 2028.

5) OTT licensing agreements will begin to standardize

One of the major pain points for content sellers distributing video media across multiple streaming platforms has been non-standard licensing agreements . As free streaming services rapidly grew in popularity over the past few years, many content sellers established new distribution deals and faced highly inconsistent licensing, payment, and data-sharing terms across the various providers. Now that many of these newer distributor relationships are entering their 2nd or 3rd year, content sellers are trying to streamline the licensing management process by pushing for more standardized distribution agreements. That includes advocating for more data rights and contractual requirements for OTT platforms to provide more complete content performance, engagement, and financial data on a regular basis.

6) Traditional pay TV will shift to an OTT delivery model

As audience viewing habits continue to shift away from traditional pay TV in favor of streaming services, MVPDs are searching for ways to stay relevant, compete with OTT offerings, and improve the viewing experience for millions of subscribers. One change we’re now seeing in MVPDs is cloud virtualization of operations: MVPDs that traditionally distributed via cable or satellite and a set-top box are shifting their playout to the cloud, making it possible for audiences to watch on CTV devices or mobile apps without a set-top box. Switching to OTT delivery makes sense for MVPDs. Consumers can access pay TV directly from the app screen with no “input switching,” and MVPDs can spend fewer resources installing and servicing set-top boxes. Another aspect of this OTT video trend is the release of pay TV streaming devices, especially the new Xumo Stream Box from Comcast and Charter. The device connects to CTV devices and offers the Spectrum TV streaming app with support for hundreds of other SVOD and ad-supported streaming options. Throughout 2024, we expect to hear more about traditional MVPDs releasing streaming apps and devices to strengthen their presence in the OTT space.

7) Streaming services will focus on international markets

The U.S. streaming market is nearing saturation, with more than 377 independent OTT streaming providers and a market penetration of ~85%. With slowing domestic subscriber growth and high rates of churn, streaming services are increasingly looking at the international market as the most important frontier for business growth. For streaming services, focusing on international markets means distributing more localized and foreign-language content - and that’s exactly what we’re seeing. Apple TV+ recently ordered its first Russian language original, and Disney Plus is in the middle of an ambitious plan to release 20+ new titles for the East Asian market by July 2024. Meanwhile, Amazon Prime Video is focused on the Indian market with a huge selection of films in Hindi (respondents to 3Vision’s 2023 TV Industry Trends & Predictions Report ranked the Indian market #1 for future growth prospects).

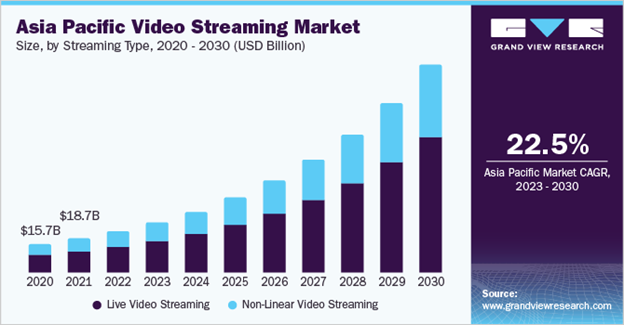

The Asia Pacific Video Streaming Market is expected to grow at a compound rate of 22.5% over the next seven years. (Source) With the focus on international markets, 2024 will bring new opportunities for overseas content sellers to enter mutually beneficial content distribution deals with major streaming service providers.

8) AI solutions will see widespread adoption across all aspects of the video ecosystem

Artificial intelligence is playing a transformative role throughout the media production and distribution ecosystem. The most data-driven content producers, marketers, and distributors are leveraging AI-driven software tools to:

- Automate tasks like scriptwriting and video editing

- Deliver personalized viewing recommendations to streaming audiences

- Generate subtitles or dubbing at scale and across multiple languages

- Accelerate video file transfer to enhance the streaming experience

- Enhancing metadata to better understand audience preferences and viewing habits

- Efficiently manage OTT licensing agreements at scale

- Analyze OTT content performance, audience engagement, and financial data to help content sellers optimize content distribution.

AI has numerous applications in the media industry, and we expect to see a significant increase in AI adoption through 2024 and into the future.

9) TikTok will expand into horizontal screen and long-form content

TikTok is one of the world’s most popular content sharing platforms, with kids and teens now spending more time watching TikTok than YouTube. The social media giant is now seeking to compete in the OTT streaming arena by unlocking features to help creators deliver longer, more engaging content for larger screens. The first change in this direction came when TikTok started allowing creators to publish videos up to 10 minutes in length. Now, TikTok has released a horizontal/full-screen mode that enhances the viewing experience on mobile devices. TikTok’s TV app will be used to translate that full-screen viewing experience onto connected TVs, enabling TikTok to compete directly with video-sharing AVODs like YouTube and free streaming providers like Tubi and Xumo.

10) OTT data management complexity will increase for content sellers

The process of aggregating, normalizing, and analyzing OTT platform data to extract insights has become increasingly challenging for content sellers. Each OTT platform has unique tracking capabilities and reporting requirements, so content sellers frequently receive data sets that vary wildly in format, quantity, and frequency. The absence of an industry-wide data-sharing standard makes it difficult for content sellers to compare data between platforms – or obtain it at all in some cases. Plus, not only are there more OTT platforms than ever before, but many of them also offer multiple distribution formats. Hybrid free platforms offer FAST and AVOD, and subscription-based platforms increasingly offer ad-free and ad-supported tiers. This means that content sellers can have multiple distribution agreements with each platform – one for each monetization format. The result of this OTT video trend is that content sellers are inundated with huge volumes of non-standardized OTT platform data that must be aggregated and normalized before it can be analyzed and understood. To overcome the growing complexity of OTT data management in 2024, content sellers can look to software solutions like Revedia that can automate the process of aggregating, normalizing, and analyzing OTT platform data at scale.

Manage OTT streaming revenue in 2024 with Revedia

Ready to upgrade your media data management in 2024? SymphonyAI’s Revedia Platform is designed to manage, optimize, and predict revenue and content performance across all digital and linear platforms. With Revedia, content sellers can combine data from multiple platforms for a single source of truth to ultimately help maximize licensing revenue. To see Revedia in action, watch the webinar Growing AVOD & FAST Revenue with Revedia.