The Three Biggest Distribution Trends Set to Hit EMEA in 2023

Last year did not see much easing of the disruption to the EMEA TV industry. New services emerged and stole market share from titans like Netflix, which are seemingly hitting their growth limit. This isn’t just true of the entertainment industry, as a mass tech sell-off risks shrinking much of the value attached to Silicon Valley.

Radical change is expected to continue in 2023, either out of a necessity for survival from established players or from new entrants to the fray setting out to disrupt the current status quo in their favor. There are many ways the entertainment industry in EMEA might swing in 2023, but these are three of the largest shifts most likely to occur.

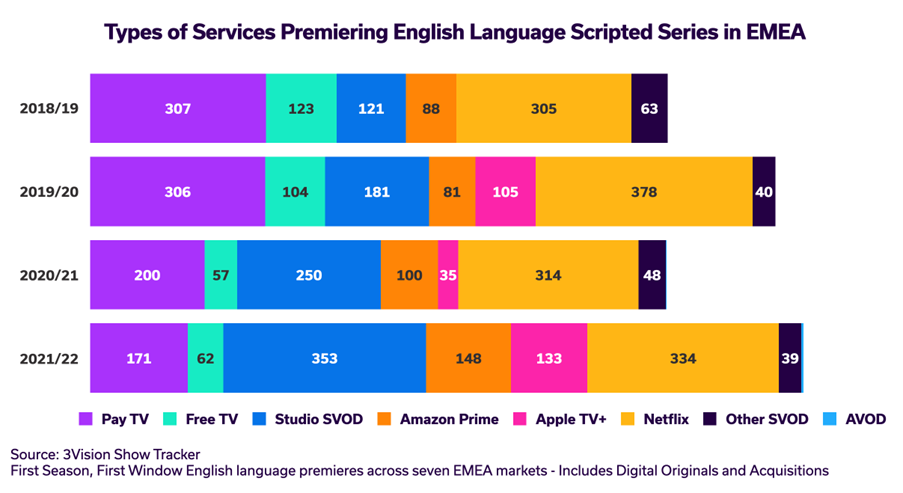

1) Studio SVOD will premiere more Scripted TV than the Silicon Valley Streamers

Over the past few TV seasons, the number of premieres on US Studio-owned SVOD services has grown substantially across EMEA. This has been fuelled by the rollout of those services to new markets (gradual for some like HBO Max, rapid for others like Disney+), a surge in the number of digital originals produced for those services and increased acquisition of scripted content from third-party suppliers.

This latest season was the first time Studio SVOD premieres overtook the huge number of premieres from Netflix, which largely stems from its own original productions. While the number of premieres from the likes of Apple TV+ and Amazon Prime continued to grow, 2023 will see Netflix taking a more restrained approach to content production in response to their dramatic bleed of subscribers earlier in 2022. This, combined with Netflix’s reduced acquisition activity of new TV series over the years, will likely result in a heavy retraction in the number of premieres compared to previous seasons.

Studio SVOD original production will continue to rise, with more Studio SVOD launches, such as the long-awaited SkyShowtime joint venture between Paramount and NBCUniversal. With these factors, it seems very likely that Studio SVOD premieres will overtake the traditional streamers in 2023. This trend will be amplified even further by our next prediction for the year…

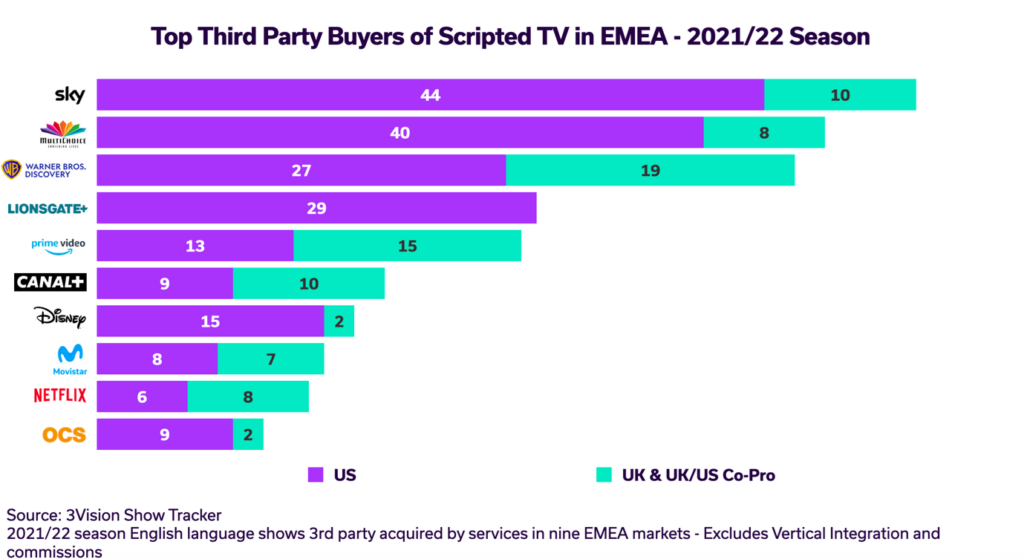

2) Studios will become EMEA’s biggest third-party buyers

While continued Studio SVOD activity brings with it the expected rise in the vertical integration of content, the multi-market prevalence of Studio SVOD services also makes them very attractive buyers for third-party distributors looking to sell their series at a high price to multiple markets quickly. In the most recent TV season, three US studios (notwithstanding Sky, itself owned by NBCUniversal) made it into the top ten third-party buyers in EMEA.

The multi-market presence of Sky in Europe, with its many historical volume deals, puts the NBCU-owned Pay TV operator at the top of the ranking, followed shortly by Multichoice, whose domination in South Africa as a buyer is fuelled by content acquisitions for both their M-Net channels and SVOD Showmax. The historic volume deals that have propped up a lot of the Sky catalog over the years from Warner and Paramount are safe for the time being, but their long-term future is more uncertain.

Warner’s HBO Max was always a prevalent buyer of third-party content when it existed in markets like Spain and Sweden as HBO España and HBO Nordic, but since its brand unification HBO Europe has increased its buying activity, with particular attention on series coming from the UK.

Lionsgate+ (formerly StarzPlay) has also held steady acquisition numbers over the years, with its ubiquitous presence in EMEA helping to keep it high up in the top third-party buyers as it sought to supplement its Starz originals slate with premium drama series. Lionsgate’s spin-off of Starz will likely result in pressure for the international SVOD to acquire even more third-party content.

Other traditionally active Pay TV operators are not seeing as many premieres as other seasons. Canal+ (with operations in both France and Poland) has been beaten out by both Warner and Lionsgate, while only remaining inches ahead of Disney+ last season.

While Sky and Multichoice shouldn’t see any major drops in premieres in 2023, Warner and the other studios are gaining in terms of their buying activity and distributors are starting to take notice. It is very likely HBO Max may sneak ahead of either Sky or Multichoice next year (or both), but at the very least as a combined presence, the Studio SVODs will start to trump the buying power of the traditional Pay TV titans. If broadcasters can’t compete in sheer volume, they will need to find other ways to level the playing field against SVODs, leading to our final prediction.

3) Broadcasters will prioritize their Digital Footprints

The dominance of SVOD services from both Silicon Valley and Hollywood means that on-demand is no longer a nice-to-have enhancement for broadcasters, but a must-have. The past few seasons have seen EMEA broadcasters acknowledge this, as more and more TV series have seen entire seasons be made available on digital-adjacent catch-up services.

Even Free TV is engaging in stronger levels of enhanced catch-up than in previous years, as their digital-adjacent catch-up services now begin to morph into essentially AVOD services unto themselves. 17% of Pay and Free TV acquisitions last season went straight to broadcasters’ digital spaces with no linear premiere, showing the focus broadcasters are putting into their digital presence. As even those appearing on linear are getting stacked (or dropped all at once) on broadcaster AVOD, the digital footprint of a linear debut remains enhanced.

Pay TV meanwhile has held historic highs in enhanced catch-up, as anyone paying a subscription will always expect a decent on-demand presence. It has, however, crossed over less into the digital-only release space, not willing to compromise the importance of the linear premiere as a subscriber event unto itself.

It remains more important than ever to not only stay on top of the 2023 media and entertainment trends, but to do so in a way that translates data into a solid business strategy.