SymphonyAI Summit acknowledged as an Honorable Mention in the 2022 Gartner Magic Quadrant for IT Service Management Tools report by Gartner.

Magic Quadrant for IT Service Management Platforms

ITSM platforms offer workflow management and related insights that let organizations design, automate, manage and deliver integrated IT services and digital experiences. This research profiles vendors in the enterprise ITSM platforms market to help I&O leaders align them with their IT roadmaps.

Market Definition/Description

This document was revised on 1 November 2022, and again on 28 November 2022. The document you are viewing is the corrected version. For more information, see the Corrections page on gartner.com.

IT service management (ITSM) platforms offer workflow management and related insights that enable organizations to design, automate, manage and deliver integrated IT services and digital experiences.

Core capabilities include:

IT support enablement through embedded incident, problem and knowledge management

Request management

Multichannel engagement of users (e.g., portal, mobile, virtual agent, live chat, walk-up)

Adaptive change and release management

Service configuration management

Service reporting and resource management

Integrated AI for automated and assisted insight

Workflow, automation and integration between IT/enterprise service management management (ITOM) tools, development tool chain and service providers

A wide range of organizations use ITSM platforms. While not required to be a vendor in this defined market, tools may also offer extended capabilities in the form of embedded functionality or support for native integrations. This extended functionality may include:

Case management, to facilitate simple ticketing and workflow requirements of business units adjacent to IT.

A graphical process designer, to create and manage workflows.

Digital employee experience (DEX) management functionality.

Native discovery and dependency mapping for configuration management.

IT/enterprise service management event alerting and communication.

ITSM platforms are typically acquired as a subscription via SaaS, but are also sold as on-premises deployments or containerized solutions. Infrastructure and operations (I&O) leaders select solutions to be consumed by service desks, service operations teams and the product teams they support, as well as for business workflow administration in other IT-adjacent departments.

Magic Quadrant

Vendor Strengths and Cautions

Atlassian

Atlassian is a Leader in this Magic Quadrant. Its ITSM platform is Jira Service Management. Atlassian’s strategy is aimed at providing a single platform that connects development, I&O and business teams. Atlassian targets organizations of all sizes for ITSM. Its recent acquisitions include Percept.AI for virtual agent technology in 2022, and ThinkTilt for form design in 2021. In late 2020, Atlassian announced the end of life of its Server Edition product, requiring customers to migrate to its cloud offering or purchase a separate Data Center license.

Strengths

Product innovation: Atlassian has a differentiated vision of the ITSM platforms market, driven by its development experience, which is focused on product-centric thinking, federated ITSM models and collaboration. Atlassian invests a large percentage of its revenue into R&D. Compared to competitors of equal size, Atlassian has a relatively large number of ITSM-related patents to protect its intellectual property (IP).

Targeted acquisitions: Through a number of targeted acquisitions, Atlassian has been able to rapidly enhance its ITSM platform capabilities in areas such as form design and configuration management. In particular, its acquisition of Percept.AI has enabled it to feature native virtual agent technology on its short-term roadmap.

New customer growth: In 2021, Jira Service Management was the fastest-growing product by new customer count among all offerings from the vendors evaluated in this report. Atlassian’s new customers range from small businesses to those with more than 5,000 licensed users.

Cautions

Account management: Atlassian’s account management efforts are largely focused on larger, more strategic accounts. Smaller customers have raised concern about the quality and availability of account management, direct implementation services and direct customer success support.

Product gaps: With its focus on DevOps, Atlassian has not addressed some of the gaps in its Jira Service Management product with regard to traditional IT support. The solution still lags behind more advanced tools in some critical capabilities, including the ability to fully support multichannel engagement models and reporting. These gaps will limit the vendor’s ability to fully displace incumbent ITSM platforms among more mature customers.

Vertical market focus: Atlassian lacks industry-specific functionality and marketing as part of its platform strategy. Jira Service Management Cloud’s lack of HIPAA (planned for late 2022) and FedRAMP compliance requires some regulated verticals, such as healthcare and government, to purchase more expensive Data Center licenses to support on-premises deployments.

BMC

BMC is a Leader in this Magic Quadrant. Its ITSM platforms are BMC Helix ITSM, BMC Helix Remedyforce and Footprints, of which its flagship offering is BMC Helix ITSM. Accordingly, that is the product used to evaluate BMC’s product score in this report. BMC’s strategy is aimed at unifying operations and service management to better support DevOps teams and connect the lines of business. BMC primarily targets BMC Helix ITSM at midsize to large enterprises. For smaller organizations, BMC leads with its other ITSM products, BMC Helix Remedyforce and Footprints. In 2021, BMC acquired StreamWeaver to improve its AIOps and observability, and ComAround, in 2020, for knowledge management.

Strengths

Advanced service operations capabilities: BMC Helix ITSM supports the needs of highly mature I&O organizations with strong ITSM process support, BMC Helix Operations Management integration for monitoring and observability, robust configuration management and AI-driven features such as incident clustering.

Enterprise experience: BMC has a long history of supporting the needs of larger enterprises with an extensive partner network, direct account management and customer success teams.

Global presence: BMC’s customers are geographically distributed, supported by a broad set of local offices, partners in each major region and worldwide hosting choices on Amazon Web Services (AWS; including FedRAMP), Azure and BMC Cloud. The latter has data centers in North America, Europe, the Middle East and Asia/Pacific.

Cautions

Reliance on technology partners: BMC has partnered with other vendors for some features (e.g., BMC Helix iPaaS and BMC Helix Dashboard, as well as some AI capabilities, including the BMC Helix Virtual Agent), rather than acquiring or building this technology directly. The nonproprietary nature of these features makes it harder for BMC to differentiate itself from many of its competitors in these areas.

Advanced Feature Pricing: Some advanced features require additional licenses and subscriptions. These include BMC Digital Workplace Advanced (which supports native live chat, appointment scheduling and location support), as well as the virtual agent, AIOps and out-of-the box connectors with iPaaS within BMC Helix. With those additions, BMC Helix ITSM has one of the highest combined list license costs of all the offerings from vendors evaluated in this Magic Quadrant.

Product complexity: Despite BMC’s 2020 acquisition of Alderstone to support customer implementation and migration initiatives, customers still find the product to be complex. As a result of this complexity, substantial resources are required to support the platform, slowing down the enablement of new features.

EasyVista

EasyVista is a Niche Player in this Magic Quadrant. Its ITSM platform is EV Service Manager. EasyVista’s strategy is aimed at making it simple to set up and obtain value quickly in IT service support and delivery with integrated ITSM and IT/enterprise service management management (ITOM) products. EasyVista primarily targets midmarket organizations. In 2021, EasyVista acquired Coservit for IT monitoring and Goverlan for remote management support. In 2022, EasyVista acquired Itexis for digital experience monitoring.

Strengths

Newly acquired capabilities: EasyVista’s recent acquisitions provide it with a set of broader native operations products that complement the ITSM platform with digital experience, infrastructure monitoring and endpoint management support.

Customer relationships: In 2021, EasyVista launched an initiative to build closer relationships with its customers by aligning implementations on its platform with ITSM maturity growth. This addresses a common need among buyers who are looking for vendor support in maturing their practices.

Vertical alignment: EasyVista strategically targets specific verticals, including healthcare, education and the public sector, where its value-based strategy aligns with buyer requirements. The vendor supports HIPAA compliance for healthcare and integration with common vertical technology, such as EPIC for healthcare and Blackboard for education.

Cautions

Immature line-of-business support: While EasyVista does provide some free line-of-business extensions, it lacks a mature platform strategy and product roadmap related to case management in areas outside IT.

Lacking product differentiation: EasyVista struggles to differentiate its product in this market. Features added over the past 12 months, such as enhanced collaboration and reporting templates, are relevant, but do not differentiate EasyVista’s offering from comparable ITSM platforms.

Limited global presence: EasyVista’s market presence, new customer acquisitions and partner network are weaker outside its target regions of Western Europe and North America.

Freshworks

Freshworks is a Challenger in this Magic Quadrant. Its ITSM platform is Freshservice. Freshworks’ strategy is aimed at providing a simple and cost-effective ITSM platform that delivers modern employee experiences by leveraging integration with the broader Freshworks ecosystem of CRM and CX solutions. Freshworks primarily targets small to midsize organizations. In late 2021, Freshworks introduced workflow integration between its Freshdesk CRM product and Freshservice ITSM platform.

Strengths

Strong mind share: Freshworks maintains strong awareness among ITSM platform buyers and frequently shows up on Gartner client shortlists. This mind share is supported by a multichannel marketing approach that includes in-person roadshows, events and social media.

High midmarket growth: By providing a simple-to-use ITSM product and flexible licensing tiers, with bundled features such as orchestration and alert management, Freshservice maintains strong growth in the midmarket. In 2021, Freshworks was among the top vendors within this evaluation for both overall revenue growth percentage and new customer growth.

Fast update cadence: Freshworks offers monthly updates for its Freshservice product, enabling it to introduce new features at a quicker pace than many of its competitors in this market. All customers are upgraded automatically with each release, granting customers the ability to toggle when to enable the new features.

Cautions

Low product strategy differentiation: The product roadmap for Freshservice is largely composed of enhancements such as case management templates, broader collaboration support and process enhancements. These features, while relevant, will not help provide strategic differentiation of its product in this market.

Limited enterprise presence: While Freshworks positions its ITSM platform for companies of all sizes, the majority of new customers remain small to midsize organizations.

Immature partner ecosystem: While a significant portion of Freshservice’s sales are direct rather than through partner channels, the vendor lacks a mature segmentation approach for its partners. This limits their ability to grow into new markets by leveraging partner expertise such as in targeting larger and more mature customers or specific verticals.

IFS

IFS is a Niche Player in this Magic Quadrant. Its ITSM platform is assyst. IFS’ strategy is aimed at extending ITSM across multiple engagement channels, augmented by a broader set of ITOM and line-of-business extensions. IFS primarily targets its ITSM offering at midsize to large enterprises. In June 2021, IFS completed the acquisition of Axios Systems for its service management capabilities and to integrate into its portfolio of field service management, enterprise asset management (EAM) and ERP products.

Strengths

Cross-product extensibility: IFS’s acquisition of Axios provides it with broad platform potential to execute its strategy of extending Axios’ native ITSM and ITOM capabilities to IFS’ other EAM, ERP and CRM solutions.

Global reach: IFS maintains a broad global reach, with local offices and reseller and implementation partners in each major region (North America, Latin America, Europe, Middle East and North Africa, and Asia/Pacific). It is one of the few vendors in this evaluation with a SaaS data center presence in the Middle East.

Customer engagement: IFS has maintained strong relationships with its customers through regular implementation health checks and global customer advisory board sessions, leading to high retention and product upgrade rates.

Cautions

One-size-fits-all pricing model: IFS customers are limited to purchasing the assyst ITSM platform as part of an all-inclusive, multiproduct pricing model themed around t-shirt sizing. This atypical approach of only offering an ELA bundle based on the total user count in the organization makes it difficult for prospective customers to compare an assyst quote with named technician proposals from competitors.

Rate of Innovation: Due to the acquisition, assyst’s 2021 update cadence has been slow, with only one major release of the product. Although major releases have since returned to biannual, these have largely lagged behind its competitors in terms of emerging features such as AI/ML, and in addressing existing customer concerns in areas such as the UI.

Minimal vertical partnership support: IFS lacks strong segmentation and management of customer relationships with partners. While it does have partners in a wide range of locations, it relies on customer size, rather than relevant product or industry experience, to determine which professional services vendors to partner with.

Ivanti

Ivanti is a Leader in this Magic Quadrant. Its ITSM platform is Neurons for ITSM. Ivanti’s strategy is aimed at providing comprehensive digital employee experiences leveraging the security, endpoint management and DevSecOps capabilities of its broader Neurons platform. Ivanti primarily targets midsize to large organizations. In March 2021, Ivanti closed its acquisition of Cherwell Software for broader line-of-business support. Later in 2021, it launched Ivanti Neurons for HR, Ivanti Neurons for Facilities, Ivanti Neurons for GRC and Ivanti Neurons for PPM.

Strengths

Strong vertical alignment: Ivanti sucessfully targets vertical industries with its product, such as government and healthcare. It supports a number of standards, including HIPAA (healthcare), and is one of only a few ITSM vendors to have obtained the U.S. government’s FedRAMP Authorized status. As part of its platform strategy, Ivanti also provides healthcare-specific workflows that discover and profile medical devices and “internet of medical things” devices.

Extended product portfolio: Ivanti offers a number of differentiating features through the native integration of its adjacent solutions, including products for unified endpoint management, vulnerability and patch management, self-healing, real-time device discovery and DEX.

Line-of-business expansion: The acquisition of Cherwell provides Ivanti with line-of-business workflow support with a broader library of built-to-purpose solutions, including Ivanti Neurons for HR, Facilities, Governance Risk Compliance (GRC) and Project Portfolio Management (PPM).

Cautions

Minimal customer success resources: Ivanti lacks a robust set of tools, templates and guides to help customers on their ITSM maturity journeys. Customers must rely largely on their implementation partners or Ivanti’s peer support community for this help.

Limited emerging market presence: Ivanti has limited customer references and resources to support customers in emerging markets within Asia/Pacific, Latin America and the Middle East, challenging its growth ambitions and competitiveness in those regions.

ITOM and DevOps Gaps: Ivanti’s focus on its three pillars of endpoint, security and service management leave it exposed against vendors with broader ITOM- and DevOps-oriented messaging and functionality. For example, as of our evaluation, Ivanti lacks ML to dynamically identify the risks associated with changes, and only has out-of-the box integrations with a small set of common monitoring and observability tools.

ManageEngine

ManageEngine, a division of Zoho, is a Challenger in this Magic Quadrant. Its ITSM platform is ServiceDesk Plus. ManageEngine’s strategy is aimed at providing ITSM as part of a broad portfolio of integrated IT and business management products. ManageEngine primarily targets small to midsize enterprises. In late 2021, ManageEngine introduced a new release management module and extended its AI capabilities to its on-premises customers.

Strengths

Low price: ManageEngine is one of the most affordable ITSM offerings evaluated in this research, with several pricing tiers that lower the cost of entry and enable customers to grow. The affordable pricing aligns well with the needs of ManageEngine’s target midmarket customers, as well as larger, value-oriented customers.

High growth: With flexible deployment models and effective positioning in the midmarket, ManageEngine was among the top vendors within our evaluation for both revenue growth percentage and new customer growth in 2021. While the majority of its new customers are midmarket, ManageEngine has been able to demonstrate large enterprise growth.

Broad product portfolio: ManageEngine offers a broad portfolio of complementary products, including endpoint management, network monitoring, application monitoring and active directory management solutions. Along with the low-code development and line-of-business integrations offered through its parent company, Zoho, these products provide the vendor with a broad set of platform capabilities and cross-selling opportunities

Cautions

Low product innovation: ManageEngine’s roadmap largely focuses on process enhancements, integrations and customization support, which are largely catch-up in nature. While the vendor has introduced some AI/ML capabilities over the past 12 months for field and template recommendations, it still lags behind more advanced products in this category.

Undifferentiated ITSM marketing: ManageEngine does not consistently highlight clear ITSM differentiation in its marketing. By focusing on commonplace themes such as low-code development, customer privacy and deployment flexibility in its marketing, the vendor will struggle to stand out to more mature buyers in this market.

Limited integrations beyond the Zoho ecosystem: Platform integrations and extensibility are at their strongest when combined with other products from the ManageEngine and Zoho ecosystem, whereas customers may be forced to build custom API connections to many other popular ITOM tools.

Micro Focus

Micro Focus is a Niche Player in this Magic Quadrant. Its ITSM platform is Service Management Automation X (SMAX). Micro Focus’ strategy is aimed at providing an extensible service management platform with simple, affordable, fit-for-purpose ITSM and ITAM capabilities, expanding to other lines of business. Micro Focus primarily targets small to midsize enterprises.

On 25 August 2022, OpenText announced its intention to acquire Micro Focus. At the date of publication, Micro Focus met the inclusion criteria for this Magic Quadrant and continued to operate as an independent entity. Gartner will provide additional insight and research to clients as more details become available regarding the acquisition.

Strengths

AI/ML adoption: Micro Focus bundles its AI/ML capabilities for its customers at no additional cost. This lowers the barrier to adoption and has resulted in the majority of its SMAX customers using some AI/ML features to augment their ITSM practices. The vendor expanded this functionality in 2022 with new ML-based expert recommendations for ticket handling.

Ease of administration: Micro Focus has designed its product to enable codeless configuration, and continues to expand its codeless integration capabilities. These address a key challenge among buyers to reduce implementation and upgrade time and ongoing administrative resource requirements.

Pricing flexibility: Micro Focus makes it easy for its SMAX customers to switch between named and concurrent licensing mid-contract with a flexible, unit-based model. Micro Focus also offers a limited number of Operations Orchestration, Software Asset Management and Universal Discovery licenses at no cost.

Cautions

Decreased revenue: While SMAX, as a new product, is gaining customers, both Micro Focus and its overall ITSM portfolio have seen annual decreases in revenue since 2019. This lower revenue limits the funds that can be directly reinvested into the product.

Vertical focus: Micro Focus lacks industry-specific functionality as part of its platform strategy. It also lacks support for industry-specific regulatory standards, including HIPAA, FedRAMP Authorization (part of its roadmap) and PCI, which limits the product’s appeal in industries such as healthcare and the U.S. government.

Product roadmap gaps: While it is investing in new AI/ML features and making the platform easier to manage, Micro Focus’ long-term product strategy lacks plans for enhanced practice support and differentiation.

ServiceNow

ServiceNow is a Leader in this Magic Quadrant. Its ITSM platform is named IT Service Management. ServiceNow’s strategy is aimed at providing a single platform with a broad portfolio of IT and line-of-business applications to help customers manage workflows across their organizations and departments. ServiceNow primarily targets larger organizations. In 2021, ServiceNow acquired DotWalk, which automates upgrades and testing of ServiceNow applications. It also acquired Swarm64 for scale, observability vendor Lightstep, indoor location vendor Mapwize and RPA vendor Intellibot. In 2022, ServiceNow acquired Hitch Works for skills mapping and Era Software for observability and log management.

Strengths

New product enhancements: Through a combination of platform-focused acquisitions and native development, ServiceNow is releasing more native advanced features than any other vendor in this evaluation. It maintains a number of advanced product differentiations, such as native process mining and workforce optimization, and has a clear 18-month product roadmap.

High platform adoption: ServiceNow effectively markets and sells across its broader platform and extended ITSM capabilities to its customers. Gartner regularly sees customers purchasing products beyond ITSM to extend their platform utilization in areas such as HR, CEC, GRC and broader ITOM, and ServiceNow’s revenue for ITSM in 2021 was over three times that of its closest competitor.

Market presence: ServiceNow has strong relevance to ITSM customers, as measured by our market momentum index, which includes Gartner inquiries, social media and web search trends. ServiceNow maintains a strong community of users, as prospective customers regularly cite awareness or experience through their peers.

Cautions

High cost of add-ons: Customers who fail to budget for the necessary add-ons and product upgrades often encounter unwelcome costs when looking to add additional platform capabilities such as custom apps, ITOM features, line-of-business applications, orchestration, AI/ML or additional workflow approvers. These additional licensing expenses can ultimately limit customers’ ability to achieve their long-term platform goals.

Limited emerging market presence: ServiceNow has a limited presence in some emerging markets, with fewer local offices, no hosting presence in the Middle East and only a single paired data for Central and South America, located in Brazil. This will limit its growth ambitions in these markets.

Renewal leverage concerns: ITSM platform buyers frequently cite concerns that ServiceNow’s market dominance is hurting their ability to renegotiate their contracts or reduce their ServiceNow footprint without heavily impacting their current discounts.

SysAid

SysAid is a Niche Player in this Magic Quadrant. Its ITSM platform is named SysAid. SysAid’s strategy is aimed at providing core ITSM capabilities on a low-code platform that drives more automation and orchestration across business applications and processes. SysAid primarily targets midmarket organizations. In 2022, SysAid introduced a series of out-of-the-box automation scripts called “ABots” to improve its orchestration platform.

Strengths

Midmarket focus: SysAid has a clear focus on the midmarket, where it can best position its low overhead, ease of configuration and additional features beyond ITSM, such as endpoint patching and remote control.

Vertical marketing success: SysAid effectively targets key verticals, including education, healthcare and manufacturing, with vertical-specific webpages and other marketing collateral, as well as special bundling and Chromebook support for education customers.

Customer relationships: SysAid provides a number of customer enablement services at no cost, including “boot camp” day-long training sessions, health checks and service benchmarking.

Cautions

Lack of advanced ITSM capabilities: Despite SysAid positioning itself as an ITSM tool for all maturities, it lacks advanced capabilities in change management, configuration management, multichannel engagement and integrated AI. This limits the appeal of SysAid to customers with basic ITSM needs.

No line-of-business support: SysAid is the only vendor in this evaluation to lack any out-of-the-box workflow support for line-of-business applications beyond IT. This puts it at a significant disadvantage when buyers are increasingly looking for a more flexible platform.

Small vendor: SysAid has the smallest company revenues of all vendors in this Magic Quadrant, and growth in customer numbers and revenue has lagged behind the company’s midmarket-focused competitors.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor’s appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Gartner reviews and adjusts inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor’s appearance in a Magic Quadrant one year and not the next does not necessarily indicate that Gartner has changed its opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

There are no new vendors in this Magic Quadrant.

Dropped

USU was dropped, as it was not in the top 20 vendors within Gartner’s market momentum index ranking.

Inclusion and Exclusion Criteria

To qualify for inclusion, vendors need to meet all of the following criteria:

The product version considered as part of this evaluation must have been generally available by 1 June 2022.

- The ITSM platform product must include native functionality for:

- IT support enablement through embedded incident, problem and knowledge managementRequest managementChange and release managementService configuration managementService reportingMultichannel engagement of users (e.g., portal, mobile, virtual agent, live chat, walk-up)A process designer to create and manage workflow, automation and integration

The vendor must have demonstrated ongoing development of the product, with at least one major update or release (not including security updates and minor feature updates) over the past 12 months (since 1 June 2021).

The vendor must have run at least one marketing campaign for the product in 2021. The marketing campaign must have defined objectives, target audience, content and channels.

The product must have at least six new paid customers, added during 2021, with either 300 active named user licenses or 100 active concurrent user licenses for ITSM. At least one-third of customers must be using versions of software across the ITSM product portfolio that are less than 18 months old (released after 1 December 2020).

- The vendor must rank among the top 20 organizations in the market momentum index defined by Gartner for this Magic Quadrant. Data inputs used to calculate ITSM platform market momentum include:

- Job vacancies advertised on the vendor’s website.Job postings mentioning the ITSM platform, aggregated from a range of employment websites.Number of followers of the vendor on social media services.Public search engine trends referencing the vendor or their product in this market.Gartner customer search and inquiry volume and trend data, including shortlists.

- The vendor must have a sales presence or partner network that includes at least two offices (regional office or reseller partner) and new ITSM platform customers in 2021 in each of three or more of the regions listed below. In addition, at least 15% of the vendor’s ITSM revenue must be derived from outside a single region.

- North AmericaLatin AmericaWestern Europe, Eastern Europe and EurasiaMiddle East, North Africa and Sub-Saharan AfricaMature Asia/Pacific, emerging Asia/Pacific, Greater China and Japan

Honorable Mentions

There are hundreds of ITSM vendors in the market.1 While this research identifies 10 vendors that have met our inclusion criteria, a vendor’s exclusion does not mean that it and its products lack viability. Gartner regularly advises clients to also consider ITSM vendors not found in this Magic Quadrant. Below are several noteworthy vendors that did not meet all inclusion criteria, but could be appropriate for clients, contingent on requirements. All vendors listed below were among the top in our market momentum index, but did not meet other criteria.

AISERA

AISERA provides several ITSM capabilities as part of its broader portfolio of ITSM, AIOps and conversational agent solutions. Its Conversational ITSM product aims to deliver AI-enabled ITSM through conversational interfaces (e.g., chat, email) and its AISERA Next-Gen ITSM product supports ITSM for more traditional interfaces such as portals. AISERA targets midsize and large enterprises in North America, Europe and Asia/Pacific. While AISERA provides an ITSM platform, it did not meet some ITSM platform marketing and functional requirements.

Broadcom (CA)

Broadcom’s CA Service Management product is focused on providing core ITSM capabilities, integrated into Broadcom’s broader suite of enterprise software products. Its customers are primarily subscribers to Broadcom’s broader set of solutions leveraging a broader enterprise licensing agreement. Broadcom did not meet the product marketing requirement to satisfy Gartner’s inclusion criteria for this Magic Quadrant.

IBM

IBM’s Maximo Control Desk product is focused on extending its ITSM capabilities with deeper enterprise asset management integration. It is targeted at organizations of all sizes and those looking to bridge ITSM with OT management needs. IBM did not meet the product development, marketing or customer size requirements to satisfy Gartner’s inclusion criteria for this Magic Quadrant.

Salesforce

In March 2021, Salesforce announced a partnership with Tanium to deliver its IT Service Center as part of its Employee Service offering, with the aim of delivering a modern employee experience for the all-digital world and empowering IT agents to quickly resolve problems. It is targeted at existing Salesforce customers, looking primarily at IT service desk support. Salesforce did not meet the global presence requirement to satisfy Gartner’s inclusion criteria for this Magic Quadrant, as all current customers of this product are located in one region.

SolarWinds

SolarWinds complements its portfolio of ITOM and security tools with its ITSM product, SolarWinds Service Desk. It aims to provide an easy-to-use ITSM tool that is integrated into its broader software portfolio. Its customers are primarily midsize organizations. SolarWinds did not meet the minimum requirement for the number of large new customers in 2021 to satisfy Gartner’s inclusion criteria for this Magic Quadrant.

SymphonyAI (SymphonyAI Summit)

SymphonyAI Summit, a division of SymphonyAI, is focused on providing service management and automation to address the needs of IT and adjacent lines-of-business, including HR, contract management, facilities, procurement and project management. It aims to provide AI-powered IT and enterprise workflows that simplify work and increase enterprise productivity. Its customers are primarily in Asia/Pacific and North America. SymphonyAI Summit did not meet the minimum requirement for the number of large new customers in 2021 to satisfy Gartner’s inclusion criteria for this Magic Quadrant.

TOPdesk

TOPdesk is exclusively focused on its ITSM tool, TOPdesk. Its solution aims to drive ease of use and quick implementation, while offering support for other non-IT workflows. TOPdesk’s customers are primarily located in Europe. TOPdesk did not meet the global revenue spread requirement to satisfy Gartner’s inclusion criteria for this Magic Quadrant.

TeamDynamix

TeamDynamix is focused on providing a unified work management platform for ITSM, line-of-business support and project portfolio management. It aims to provide an easy-to-use no-code ITSM tool that is integrated into its PPM and iPaaS products. Its customers are primarily in North America and it has a strong presence within the higher education space, but also sells to other industries including healthcare, financial services, and government. TeamDynamix did not meet the global presence requirement to satisfy Gartner’s inclusion criteria for this Magic Quadrant.

Evaluation Criteria

Ability to Execute

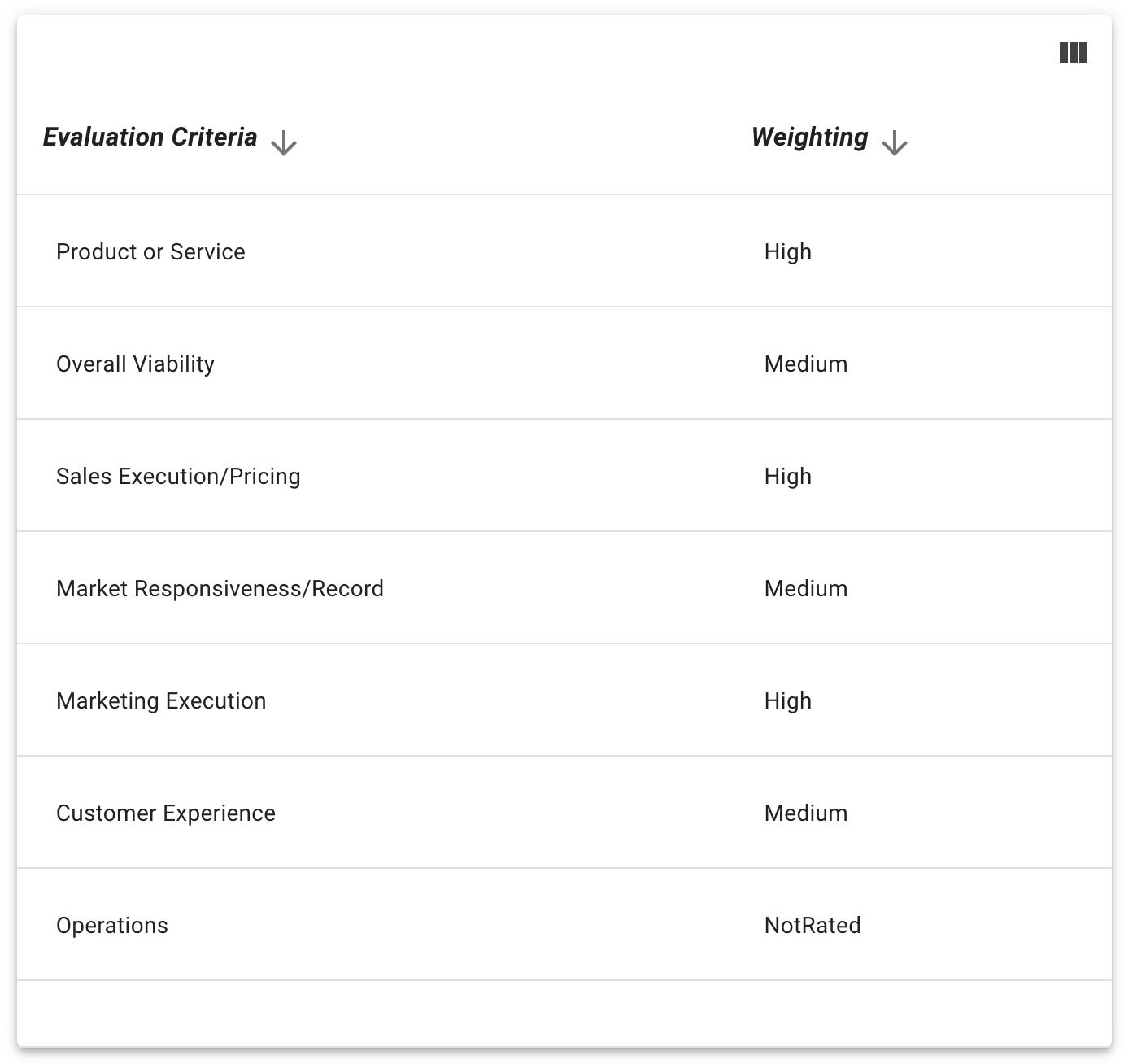

Product/Service: This refers to core goods and services offered by the vendor for the defined market. This includes current product and service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements or partnerships, as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization’s financial health and the financial and practical success of the business unit. It also accounts for the likelihood that the individual business unit will continue investing in and offering the product and will advance the state of the art within the organization’s portfolio of products.

Sales Execution/Pricing: The criterion assesses the vendor’s capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support and the overall effectiveness of the sales channel.

Market Responsiveness/Record: This refers to a vendor’s ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor’s history of responsiveness.

Marketing Execution: This criterion assesses the clarity, quality, creativity and efficacy of programs designed to deliver the vendor’s message. These programs should be aimed at influencing the market, promoting the brand and business, increasing awareness of the products and establishing a positive identification with the product/brand and organization in the minds of buyers. This “mind share” can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Completeness of Vision

Market Understanding: The vendor’s ability to understand buyers’ wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers’ wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor’s approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Vertical/Industry Strategy: The strategy to direct resources (sales, product, development), skills and products to meet the specific needs of individual market segments, including verticals.

Business Model: The soundness and logic of the vendor’s underlying business proposition.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or preemptive purposes.

Geographic Strategy: The vendor’s strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels and subsidiaries, as appropriate for that geography and market.

Quadrant Descriptions

Leaders

Leaders have executed well with broad market reach, strong customer awareness of their participation in this market, and adoption (as evidenced by Gartner client interaction data, as well as their growth and market presence). These vendors have a clear vision that addresses relevant challenges facing I&O teams. These include the impact of product teams, the need to support agile and DevOps environments, delivering impactful employee experiences, leveraging AI and machine learning to make better use of data, and collaborating in a remote or hybrid workplace. These vendors exhibit the levels of product, marketing and sales capabilities required to drive market acceptance.

Challengers

Challengers have executed well, growing market revenue, retaining good customer awareness and improving their ITSM product and overall viability levels enough to participate in the general purpose market with competitive products. In general, however, Challengers are not seen as driving the market as strongly as Leaders or Visionaries.

Visionaries

Visionaries deliver an innovative approach to the market that addresses operationally important I&O organizational challenges, such as optimizing operational efficiency and creating more agile ITSM processes. However, they have yet to execute as well as Challengers or Leaders. Visionaries have a differentiated message and product strategy that resonates with buyers’ developing needs.

Niche Players

Niche Players have strengths in particular areas of ITSM and often offer solid products for a specific use case, but generally have not invested in satisfying all the requirements to demonstrate Completeness of Vision and the Ability to Execute. The Niche Players in this Magic Quadrant focus on a small segment or are in the process of ramping up go-to-market efforts, and have yet to develop the vision to break out. Alternatively, they are scaling down their offerings by retiring products.

Context

The title of this research has changed this year from “tools” to “platforms” to reflect the growing interest and adoption of ITSM tools to support broader line-of-business case management needs. While the ability to support an organization’s ITSM practice goals remains core to this market, vendors now provide broader product extensibility as platforms to address the need for adaptable workflows that support customers’ digital business goals. Vertical strategy has also been added to the Magic Quadrant evaluation, as some vendors now address vertical needs with industry-specific workflows, certifications and marketing.

This Magic Quadrant is a multiregional analysis of vendors that have demonstrated enterprise scale. Vendors have been evaluated on their ability to sell to multinational organizations. Vendors that have been evaluated have new customers and either a sales presence or partner networks in multiple regions, including outside North America and Western Europe.

The Magic Quadrant for ITSM platforms assesses the viability of vendors and their competitive strength in this marketplace. Inclusion and evaluation criteria are based on global market position over platform features. Factors such as global strategy may not be key for I&O leaders operating in a single country or region. Sales and marketing performance help to understand the vendor’s momentum, but do not guarantee a good fit for any particular organization. Use this research to learn about a vendor’s competitiveness and focus to gain assurance that it has a solid ITSM platform strategy and the stability to compete beyond the short term.

It is important to note that this is not a direct evaluation of the ITSM products that these vendors offer. This analysis is complemented by the Critical Capabilities for IT Service Management Platforms, which analyzes eight critical capabilities that differentiate these products weighted into three use cases: service desk, service operations and business workflow automation. Gartner strongly recommends that organizations use this research in conjunction with the Critical Capabilities companion research. Organizations should also apply the selection best practices included in A Buyer’s Guide to ITSM Platforms, inquiries with analysts, Gartner Peer Insights and other Gartner research to define their requirements and select solutions that match their needs.

Market Overview

Buyers seek out ITSM platforms to offer expanded workflow management and service operations insights that enable them to design, automate, manage and deliver integrated IT services and digital experiences.

Throughout 2021, Gartner continued to observe buyer demand for functionality that extends the scope of ITSM tools beyond traditional IT service management practice support. These demands include:

Expanding service management workflows with out-of-the-box content to support line-of-business needs, such as HR and facilities case management.

Low-code and no-code workflow design capabilities, which enable citizen developers to modify ITSM process flows and build out their own custom workflows.

Broader integration into IT/enterprise service management management, line-of-business and application development tools.

While some of this demand was manufactured through vendor marketing, many vendors’ product strategies reflect a sustained commitment to providing platform extensibility. To reflect this sustained shift in buyer needs and vendor direction, Gartner has renamed the market from “ITSM tools” to “ITSM platforms.”

Although ITSM process support still remains the primary purchasing driver behind ITSM platforms, vendors will often look to differentiate their go-to-market approaches based on the needs of their buyers. Some examples include:

The majority of vendors in this market offer ITSM platforms that focus on IT service desk and ticketing functions targeted at lower-maturity I&O organizations. These vendors typically highlight the value they offer in enabling core ITSM competencies (incident management, request management, knowledge management, etc.) with low administrative complexity and inclusive pricing models. They may offer some limited applications of AI and machine learning in their solutions in areas such as predictive field recommendations. However, enhancing core process support and improving multichannel engagement (e.g., chatbots, walk-up and mobile apps) typically drive much of the product strategy.

Some vendors target highly mature I&O organizations with a greater need to support service operations through more extensive IT service life cycle management. These vendors offer deeper support for change, release and configuration management, as well as advanced automation, AI-driven insights and adaptive processes. A limited scope of vendors target emerging use cases, such as DevSecOps and DevOps, with specific integrations, workflows or ways to uncover related insights.

Most vendors support some line-of-business extensibility and market that in their offerings. However, the presence and maturity of out-of-the-box workflows, third-party tool integrations (e.g., connecting to common HR information systems) and unified experiences between them varies widely.

Evidence

1 Help Desk Tools for ITIL & Service Management, Listly.

Gartner’s community of more than 1,200 analysts engages in more than 250,000 one-on-one client interactions each year. Conclusions are based on data from Gartner interactions with Gartner clients purchasing ITSM tools collected during the past 18 months (as of 1 July 2022).

Gartner collects ITSM tool statistics from anonymized client inquiries detailing ITSM tools in use, scheduled for replacement and on shortlists for selection.

Source of social media analytics (SMA) data: Gartner conducts social listening analysis leveraging third-party data tools to complement or supplement the other fact bases presented in this research. Due to its qualitative and organic nature, the results should not be used separately from the rest of this research. No conclusions should be drawn from this data alone. Social media data in reference was gathered from 22 February 2021 through 22 February 2022 in all geographies (except China) and recognized languages.

The SMA team: Ritesh Srivastava and Ayush Saxena.

Evaluation Criteria Definitions

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization’s financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization’s portfolio of products.

Sales Execution/Pricing: The vendor’s capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor’s history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization’s message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This “mind share” can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers’ wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers’ wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor’s approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor’s underlying business proposition.

Vertical/Industry Strategy: The vendor’s strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor’s strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.