Compliance modernization - Why financial services can't afford to stand still

A strategic guide for Chief Compliance Officers navigating the transition from legacy AML infrastructure to adaptive, AI-powered compliance programs

Executive Summary

More than 70% of financial institutions report AML false positive rates above 25%, and most compliance programs spend the majority of their operational budget processing noise rather than detecting crime. The Wolfsberg Group warned in July 2025 that many programs remain “risk-based in name only.” This article sets out why legacy rule-based AML systems are structurally failing in today’s regulatory environment, what continuous risk alignment looks like in practice, and how Chief Compliance Officers (CCOs) can build a defensible business case for transformation, drawing on the FinCrime Frontier 2025–26 survey, the FinCEN June 2024 NPRM, and current FATF, FCA, and EU AML regulatory frameworks.

Introduction

The call that every CCO dreads isn’t from a regulator. It’s from their own team, telling them that a suspicious activity report (SAR) was filed three days late because the case management system went down again. Or that the transaction monitoring platform generated thousands of alerts last month, and that analysts cleared 95% of them as false positives without ever finding the pattern that would have mattered.

These aren’t edge cases.

According to the SymphonyAI FinCrime Frontier 2025–26 survey - one of the most comprehensive studies of compliance operations conducted in the past year, drawing on responses from institutions across North America and EMEA - more than 70% of financial institutions report AML false positive rates above 25%. Nearly a third face false positive rates exceeding 75%. And 54% of respondents say that fewer than 5% of their alerts ever lead to a case escalation or a suspicious activity report filing.

Put those numbers together and they tell a story that’s hard to ignore, which is that most AML compliance programs are spending the vast majority of their operational budget processing noise instead of detecting crime.

This is the compliance modernization problem. And for Chief Compliance Officers at mid-to-large financial institutions, it is no longer a technology planning exercise but an existential strategic question. Just how do you solve it?

Why legacy AML systems are breaking down

The case for BSA/AML modernization isn’t new, but the urgency has changed.

Legacy rule-based transaction monitoring systems were designed for a world of lower transaction volumes, simpler product sets, and regulatory frameworks that changed slowly. They worked when you could define a finite set of typologies in advance and tune thresholds manually.

That world is gone.

Today’s compliance environment combines the velocity of real-time payment rails like FedNow and instant payment schemes with the complexity of cross-border digital transactions, the regulatory specificity of the EU AML package (AMLA, AMLR, and 6AMLD), and the escalating expectations of FinCEN modernization initiatives, FATF mutual evaluations, and regulators in every jurisdiction demanding demonstrable effectiveness rather than checkbox compliance. If that feels like a lot, it’s because it is.

So how do legacy systems respond to this complexity? By generating more alerts. This means more thresholds. More rules. More manual review. And the compliance team, which is already stretched, absorbs the cost.

The FinCrime Frontier survey found that 65.6% of compliance professionals identify poor data quality and integration as the single biggest drag on AML efficiency. Not regulatory uncertainty or budget, but data. Fragmented customer profiles. Disconnected transaction histories. Siloed case management that forces investigators to work across multiple screens to assemble context that should be visible in a single view. In a recent Celent survey, 59% of risk and compliance executives highlighted data management as their top IT priority, which was 2% higher than AI. This is not a rebuttal of AI but a direct consequence of it.

Legacy AML system replacement is often framed as a technology conversation but that simplifies the difficulty. In truth, it’s an operational resilience conversation, a compliance cost reduction conversation, and increasingly, a regulatory risk conversation because regulators are paying close attention to whether institutions can demonstrate that their programs actually work.

The real cost of not modernizing your compliance stack

Before exploring what compliance transformation looks like in practice, it’s worth being precise about the cost of standing still.

The direct cost of alert volume is measurable. If your analysts spend an average of 20 minutes processing each alert - gathering context, reviewing transaction history, making a disposition decision, documenting their reasoning - and your platform generates 40,000 alerts a month with a 90% false positive rate, you’re allocating roughly 12,000 analyst-hours per month(!) to work that produces no investigative value whatsoever. And that’s before accounting for quality assurance, escalations, or SAR drafting.

The indirect cost of delayed detection is harder to quantify but potentially far more serious. High false positive rates don’t just waste time but create alert fatigue that degrades the quality of human judgment. Investigators who spend their days clearing obvious false positives are less attentive to an ambiguous, complex case that actually warrants scrutiny.

The regulatory cost of inadequate systems is becoming tangible. The FinCEN compliance requirements landscape has evolved significantly. Regulators are no longer satisfied with volume-based evidence of compliance activity but instead want to understand the effectiveness of detection, the quality of risk-based decisions, and the auditability of AI and model-driven processes. Institutions that cannot answer those questions confidently are increasingly exposed.

The talent cost compounds everything else. Skilled financial crime investigators are in short supply globally. Retaining experienced analysts in an environment of soul-destroying false positive volumes is genuinely difficult, especially when they can be found criminally liable for missing a financial crime. This is an ever-worsening risk for compliance operations.

The compliance modernization roadmap: Where to begin

For CCOs evaluating compliance modernization, the instinct is often to ask: “Should we replace our platform?” That’s the wrong first question and, to be honest, an extremely expensive proposition both in terms of monetary cost and how long it will take to train staff. The right first questions are:

What is our data foundation? Almost every AML transformation that delivers measurable outcomes starts with unified, entity-centric data. Where a single customer’s transactions, risk attributes, relationships, and history are connected (rather than scattered) is the prerequisite for everything else. Machine learning AML detection doesn’t work well on fragmented data. AI-powered triage is only as good as the data it’s reasoning over. If your data model treats the same customer as three different entities depending on which system you’re looking at, no technology investment will solve your effectiveness problem.

Where is manual effort concentrated? The FinCrime Frontier survey identifies Know Your Customer (KYC), Customer Due Diligence (CDD/EDD), onboarding, transaction monitoring, and SAR drafting as the most manually intensive compliance workflows. These are the areas where manual compliance process automation delivers the fastest, most measurable return. Of course, you don’t need to modernize everything simultaneously; identify the manual bottlenecks that absorb the most analyst time and start there.

What does your alert review model actually look like? Most institutions report operating a hybrid model - partially automated workflows with human review. But saying something is ‘partially automated’ covers an enormous range from systems that auto-dismiss only the most obvious low-risk alerts to programs with sophisticated risk-based triage that channels only the genuinely ambiguous cases for human review. Understanding where you sit on that spectrum is essential before evaluating next steps.

What does your regulatory examination posture require? The FATF compliance framework and FinCEN modernization guidance both emphasize the importance of risk-based approaches (RBA), demonstrable, documented risk-based decision-making that can be explained to an examiner. Any modernization initiative that cannot produce clear, auditable reasoning for how decisions are made will create as many regulatory challenges as it resolves.

AI vs. rule-based transaction monitoring: Understanding the real difference

A large proportion of the financial services compliance conversation right now centers on AI-powered compliance and machine learning-based AML detection. It’s worth being precise about what these terms actually mean and more importantly, what they mean for compliance effectiveness.

Traditional rule-based transaction monitoring operates on fixed thresholds and conditions. If a transaction exceeds a defined amount or a customer’s behavior matches a predefined pattern, this triggers an alert. The logic is transparent and auditable. The problem is that this is a static approach. Rules don’t adapt to how criminal behavior evolves, and they can’t account for context that isn’t explicitly encoded.

Machine learning-based AML detection approaches the problem differently. Rather than hard-coded rules, machine learning models identify statistical anomalies that deviate from what would be expected for a given customer segment, product type, or risk profile. They can incorporate hundreds of features simultaneously in ways that human rule-writers cannot. Alongside this, they can learn from feedback as investigators resolve cases, and, critically, they can be tuned to reduce AML false positive rates dramatically while maintaining detection sensitivity.

The evidence for this is not theoretical. The FinCrime Frontier survey found that 35% of compliance professionals who have implemented AI cite transaction monitoring as the area where they expect the most significant ROI, and this is specifically through reduced false positives, faster alert review, and improved detection quality.

But the most effective approach for most institutions isn’t to replace rules with machine learning wholesale but to deploy machine learning alongside existing rule logic, using AI to score and prioritize alerts rather than simply generating more of them. This is the risk-based approach to AML that regulators increasingly expect. It isn’t just identifying potentially suspicious activity but prioritizing investigative resources toward the cases that are most likely to represent genuine risk.

So where does agentic AI fit in?

Well, agentic AI for AML represents the next evolution of this thinking. Where traditional automation executes predefined tasks and machine learning models produce scores and rankings, agentic AI systems can reason about complex, multi-step investigative tasks autonomously, gathering entity information, assessing contextual risk factors, identifying patterns across transactions and relationships, and presenting investigators with structured, evidence-based summaries. The investigator’s role shifts from data gatherer to decision-maker.

There is a deeper strategic shift embedded in this transition that is worth naming explicitly.

Most AML programs today are risk-based in design but periodic in execution. The enterprise risk assessment is conducted annually, threat information is reviewed manually and episodically, and control updates lag emerging threats by months or years. The result is a compliance posture that answers the question, “What was our risk last year?” rather than, “How and why has our risk changed this quarter?”

Agentic AI enables what might be called continuous risk alignment. This is a fundamentally different operating model where threat intelligence is monitored and synthesized in real time, risk assessments are living documents (not annual snapshots), and controls are recalibrated as risks evolve rather than on a fixed review cycle. This is not an incremental improvement to existing AML operations. It is a redesign of the operating model and the direction that regulators, the Wolfsberg Group, and FATF are collectively pointing toward when they emphasise outcomes-based, intelligence-driven compliance.

Automated sanctions screening and watchlist management: A case study in scale

Nowhere is the gap between legacy capability and modern expectation clearer than in automated sanctions screening and watchlist management software.

The sanctions landscape has expanded dramatically in the last three years. New designations are issued all the time, existing lists are updated frequently, and the number of entities requiring screening has grown exponentially for institutions with international exposure. Customers, counterparties, beneficiaries, and intermediaries… Sometimes the lists seem endless.

Legacy name-matching logic, designed for a world of stable lists and manageable volumes, generates enormous numbers of false alerts when applied to modern sanctions environments. Investigators spend their time dismissing obvious mismatches (variant spellings, common names, date of birth discrepancies) rather than applying their knowledge to the genuinely ambiguous and perhaps complex cases that require human expertise.

One major US financial institution faced a situation where each sanctions hit required a highly manual review process that could take over 100 minutes per case when gathering transaction details, conducting entity background checks, reviewing adverse media, and documenting the disposition. By deploying AI agents trained on their own policies and procedures, the institution was able to automate entity resolution, web research, and initial triage, dramatically reducing case resolution times and allowing investigators to focus on the cases where their expertise was genuinely needed.

This isn’t about replacing humans. It’s about deploying AI automation where it makes the greatest difference.

The regulatory dimension: FATF, FinCEN, and the EU AML package

For CCOs building a compliance modernization roadmap, the regulatory context is key.

The FATF compliance framework has consistently emphasized the risk-based approach as the organizing principle of effective AML programs. The RBA requires institutions to allocate compliance resources proportionally to the risks they face. This is, in essence, an argument for intelligence-led compliance over volume-based compliance. A program that generates 40,000 alerts and processes 38,000 of them as false positives is not applying a risk-based approach. It is applying a coverage approach that satisfies the letter of compliance activity while potentially missing the substance. It’s a classic case of treating the symptom rather than the cause.

The FATF has in recent years placed increasing emphasis on moving from procedural compliance to dynamic, intelligence-led, and measurable risk mitigation in their recommendations. This message has been amplified by the Wolfsberg Group, representing many of the world’s largest banks, which warned in its July 2025 Statement on Effective Monitoring for Suspicious Activity that many programs remain “risk-based in name only,” calling for stronger public-private collaboration, smarter resource allocation, and a genuine transition to intelligence-driven, outcome-focused compliance. That is a damning indictment from the institutions closest to the problem and a clear industry signal that the gap between claimed and actual risk-based practice is widely recognized.

The US and the EU

In the United States, the regulatory direction has become more specific. In June 2024, FinCEN issued a major Notice of Proposed Rulemaking (NPRM) aimed at strengthening and modernizing AML/CFT programs across financial institutions. The proposed rule places the risk-based approach at the centre of effective compliance, requiring banks and covered institutions to conduct and maintain documented risk assessments that identify, assess, and mitigate money laundering, terrorist financing, and sanctions evasion risks specific to their own business. This is a materially higher bar than the volume-based compliance models most legacy systems were built to support. In the UK, the FCA has pushed firms toward real-time risk understanding and better use of threat intelligence, while FINTRAC in Canada modernized its supervisory framework in August 2025 to explicitly require reporting entities to integrate the 2025 National Risk Assessment into their own risk-based programs and demonstrate evidence-based risk mitigation.

The EU AML package, which comprises the new Anti-Money Laundering Regulation (AMLR), the 6th Anti-Money Laundering Directive (6AMLD), and the establishment of the new EU AMLA supervisory authority, represents the most significant structural change to European financial crime compliance in a generation. For institutions operating across EU jurisdictions, the AMLR introduces directly applicable rules on customer due diligence, beneficial ownership, and reporting obligations that cannot be addressed through country-by-country policy interpretation. AMLA will apply supervisory scrutiny to the highest-risk cross-border institutions directly.

These regulatory developments share a common theme in that they reward compliance programs that can demonstrate intelligence, risk-proportionality, and explainable decision-making. In turn, they also expose programs that rely on volume and opacity.

The FinCrime Frontier survey found that 58% of compliance professionals view upcoming regulatory changes positively - as a driver for modernization rather than a compliance burden.

It’s evident that institutions that use the EU AML package, the FinCEN NPRM, and similar national regulations as an opportunity to modernize technology and redesign compliance operations will be far better positioned than those that simply react to new requirements as they emerge.

Building the business case: AML compliance technology ROI

One of the most striking findings in the FinCrime Frontier survey is that only 28% of compliance professionals have conducted a return on investment analysis for their compliance technology investments. Somewhat alarmingly, this is despite technology and people (combined) accounting for roughly half of total compliance spending.

This is a significant governance gap.

CCOs that cannot quantify the ROI of their technology investments are poorly positioned to make the case for modernization budgets and to hold vendors accountable for delivered outcomes. As well as this, it would be difficult for leaders to demonstrate to their boards and regulators that compliance spending is well-directed.

Thankfully, there is a simple fix as the building blocks of an AML compliance technology ROI analysis are straightforward to ascertain:

Baseline measurement requires knowing your current false positive rate, your average case resolution time, your analyst headcount and fully-loaded cost, and your current rate of SAR/CTR filing relative to alert volume. If you don’t have these numbers, establishing them is itself a valuable exercise.

Target state modeling requires realistic estimates of what modernized operations could achieve. Industry evidence suggests that:

- Well-implemented machine learning AML detection can reduce false positive rates by 50–80%

- Automated triage and case assembly can reduce the time investigators spend on data gathering by 60–70%

- Agentic AI workflows can compress investigation timelines from days to hours for lower-complexity cases

Risk-adjusted value should account for the reduced probability of regulatory action that results from improving effectiveness, faster SAR filing, and more defensible documentation of risk-based decisions.

Talent and workforce value should capture the retention and recruitment benefits of shifting analyst work from alert processing to genuine financial crime investigation.

Institutions that approach compliance modernization with this level of analytical rigor typically find that the business case is compelling. They also discover that the compliance cost reduction that financial services institutions can achieve through modernization substantially offsets technology investment costs within two to three years.

The human side of compliance transformation

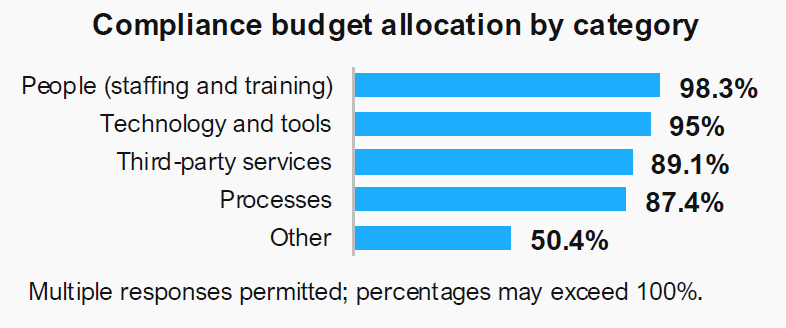

Technology undoubtedly dominates the conversation, but it would be a mistake to treat compliance modernization purely as a technology problem. The FinCrime Frontier survey found that 98% of respondents allocate significant resources to people even as automation advances. This covers staffing, training, and upskilling.

This approach is exactly right because the most effective compliance transformations aren’t just focused on the compliance but are in fact organizational transformations. They require:

Rethinking analyst roles. When AI handles initial triage, alert scoring, and case assembly, investigators have more time for the genuinely complex, judgment-intensive work that defines financial crime compliance. It requires deliberate investment in the skills that matter most in an AI-assisted environment such as critical thinking, pattern recognition, regulatory judgment, and the ability to engage effectively with AI-generated outputs.

Building model governance capability. Regulators expect financial institutions to demonstrate that they understand, monitor, and govern the AI that they are using. Despite this, the FinCrime Frontier survey found that only 17.2% of organizations have fully operational AI governance frameworks. The requirement for explainable AI models that can withstand regulatory examination is a compliance necessity.

Managing change across the organization. AML transformation touches systems, workflows, and job roles across compliance operations. Change management, training, and clear communication about why and how work is changing are as important as the technology choices that an organization makes.

Engaging regulators proactively. Institutions that proactively engage regulators and explain how AI-powered detection, model governance, explainability, and human oversight fit into their compliance modernization strategy tend to experience far more constructive examinations than those that introduce technology changes without early regulatory dialogue.

What to look for when evaluating compliance technology vendors

A CCO may have concluded that modernization of some kind is necessary, but how to assess the many options available to your organization? When it comes to evaluating AML compliance vendors, a few principles stand out:

Ask for evidence. Any vendor can claim that their solution reduces false positives or improves detection rates. Ask for specific, documented evidence from institutions at comparable scale and complexity to yours. Case studies matter while it makes sense to ignore theoretical benchmarks often seen on event booth displays.

Explainability and auditability. In an environment where FATF, FinCEN, and EU regulators expect demonstrable, auditable risk-based decision-making, any AI-powered system that cannot explain why it generated an alert, scored a case, or made a triage decision is a regulatory liability. This is non-negotiable.

Modularity and integration. Most institutions are not in a position to conduct a full legacy AML system replacement in a single program. Evaluate vendors on their ability to deliver value incrementally with AI overlays that add AI capabilities to existing infrastructure rather than requiring wholesale replacement. Not only that; it also pays to assess the vendor on the quality and flexibility of their integration architecture.

Regulatory currency. Compliance technology moves fast. The vendor you select should demonstrate active engagement with the evolving regulatory frameworks already mentioned (FATF, FinCEN, AMLA, 6AMLD, etc.) and a track record of updating their platform ahead of regulatory deadlines, not in response to them.

Model governance capability. Look for built-in model risk management, documentation, validation frameworks, and the ability to demonstrate model behavior to examiners. SR 11-7 remains the benchmark standard, and any credible AML compliance vendor should be able to articulate how their models meet it.

Framing compliance as a competitive advantage

The conventional framing of financial services compliance is as a cost center. It is a necessary function that must be adequately resourced and carefully managed but cannot itself drive business value.

This framing is increasingly wrong. Compliance transformation, done well, delivers competitive advantages that extend far beyond regulatory adherence. In this way, compliance moves from a cost center to a growth enabler.

A few examples include:

- Faster, more accurate customer onboarding. Enabled by intelligent identity verification and automated CDD, it reduces friction and improves customer experience.

- Reduced false positive volumes allow compliance teams to focus on genuine risk rather than noise, improving the quality of suspicious activity reporting and the institution’s contribution to the financial system’s defenses against money laundering and financial crime.

- Better data foundations, built to ensure compliance effectiveness, create analytical capabilities that benefit risk management, fraud prevention, and customer intelligence functions.

Institutions that build adaptive, explainable, AI-governed compliance programs are substantially better positioned to respond to regulatory change quickly and cost-effectively. The next set of regulatory requirements, whatever form they may take, will be implemented on a modern platform in weeks, not on a legacy system over months.

The compliance modernization journey is neither easy nor quick. But the institutions that begin modernizing, with clear business cases and realistic roadmaps, are building something that their peers who remain dependent on legacy infrastructure will struggle to replicate. As such, the decision is whether to start now, or to wait until the cost of not modernizing forces the decision.

Key takeaways for compliance leaders

- False positive rates above 25% are the norm, not the exception. Legacy rule-based systems are structurally incapable of resolving this at scale. Machine learning AML detection is the path forward.

- Data is the first priority. Unified, entity-centric data architecture is the prerequisite for every other element of compliance modernization. Begin there.

- ROI measurement is a governance imperative. Only 28% of institutions have measured the return on compliance technology investment. This gap creates budget risk and obscures the case for transformation.

- Regulatory requirements reward risk-based, explainable compliance. FATF, FinCEN, and the EU AML package highlight that an organization should demonstrate that their program works and can show its reasoning.

- Transformation is organizational, not just technological. People, governance, and technology must advance together. Institutions that invest in all three will set the standard.

- Start with a compliance modernization roadmap grounded in your current state. Understand your false positive rate, your manual workflow bottlenecks, your data quality gaps, and your examiner expectations before selection technology.

Related resources

From Theory to Action: AI Agents Transforming Financial Crime Compliance in Real-Time

Whitepaper: The New Financial Crime Ecosystem

Reinventing the compliance operating model

Agentic AI, Data, and Financial Crime Control

90% reduction in manual effort: The power of AI agents in sanctions compliance (Case study)

Re-engineering the Risk-Based Approach in AML compliance (Webinar)

Re-engineering the Risk-Based Approach with agentic AI (White paper)

Learn more about Symphony Risk Intelligence

Find out more about Symphony Risk Intelligence and Always-on Compliance, and how it can improve your approach to transaction monitoring, KYC/CDD, fraud, and screening.

Compliance modernization means moving from legacy, rules-based compliance infrastructure to AI-driven systems and processes that can manage financial crime risk dynamically. It covers technology, process, and operating model, not just platform replacement. Most institutions approach it in phases, augmenting existing systems with AI capabilities before committing to full migration

Legacy systems apply static rules uniformly across all customers and transactions, resulting in false-positive rates of 90 to 95 percent, meaning the vast majority of alerts are non-actionable. They also operate in silos, keeping transaction monitoring, sanctions screening, and customer risk rating disconnected. And because rule changes require IT involvement, they are slow and expensive to adapt when typologies or regulations change.

AI assesses each transaction in the context of an individual customer's behavior profile rather than applying uniform thresholds, which materially reduces false positives and improves detection of genuine risk. Models can be continuously retrained as financial crime typologies evolve, unlike static rule sets that require manual updates. Agentic AI goes further by autonomously executing multi-step workflows like alert triage, evidence gathering, and case drafting rather than simply flagging activity for human review.

A risk-based approach means calibrating controls and analyst effort to the actual financial crime risk a customer or transaction presents, rather than applying the same procedures to everyone. It is the organizing principle of FATF's international standards and is embedded in US, UK, and EU regulatory frameworks. Legacy rules-based systems cannot implement it effectively, but AI-driven platforms can, by dynamically adjusting risk scores and control intensity based on real evidence rather than static thresholds.

The strongest business cases rest on three levers:

- Cost reduction from lower false positive rates and fewer manual remediation exercises

- Risk reduction from better detection of genuine suspicious activity and stronger regulatory defensibility

- Operational resilience from platforms that are faster to tune and update than legacy systems.

A credible case also accounts for change management, since modernization involves process and workforce transition alongside technology deployment.

Henry Fosdike is Content Manager at SymphonyAI’s financial services division, bringing 10+ years of expertise in crafting compelling B2B, B2C, and D2C content to the world of AI-driven financial crime prevention technology. With a rich background, Henry excels at translating complex AI, finance, and SaaS concepts into clear, engaging narratives. His insightful articles and whitepapers demystify cutting-edge anti-financial crime solutions, providing readers with valuable knowledge and offering readers a deeper understanding of this rapidly evolving field.