Agentic AI in financial services: From hype to governance

A practical guide for Chief Compliance Officers and financial crime leaders evaluating agentic AI adoption, from concept clarity to implementation governance

Executive Summary

Agentic AI is already in active adoption among 52% of financial services firms and C-suite awareness is near-universal. The question has moved on from “what is it?” to “what does it actually change in a compliance workflow, and how do we govern it?” The gap between awareness and deployment readiness is real with only 15% of CFOs saying they are ready to deploy, citing governance, traceability, and human oversight as the primary barriers. This article focuses on those operational and governance questions, explaining what AI agents specifically do in AML, sanctions screening, and case management workflows, why that represents a structural rather than incremental change, and what a credible, regulator-ready implementation roadmap looks like. It draws on the SymphonyAI FinCrime Frontier 2025-26 survey report and the upcoming Agentic AI Leaders Guide.

Introduction

Most compliance leaders no longer need agentic AI explained to them. According to the 2026 Cambridge Centre for Alternative Finance Global AI in Financial Services Report , most at the C-suite level are aware of agentic AI and it is already in active adoption among 52% of financial services firms, with fintech leading the way at 57% and traditional institutions at 45%. The question has therefore moved on.

The more useful question (and the one this article focuses on) is why the generative vs agentic distinction still matters operationally, even for leaders who know exactly what an AI agent is. Because while adoption is accelerating, understanding of what agentic AI changes in a compliance workflow remains surprisingly shallow. A July 2025 PYMNTS Intelligence report found that despite the C-suite awareness, only 15% of CFOs expressed readiness to actually deploy agentic AI systems, citing gaps in traceability, human oversight, and governance as the primary barriers. Indeed, McKinsey’s 2026 AI Trust Maturity Survey found that only around one-third of organizations have reached meaningful maturity in agentic AI governance.

In other words, the gap is not because of understanding but because of operational and governance-related concerns or capabilities.

Why agentic AI changes compliance structurally, not incrementally

The reason the generative vs agentic distinction still matters for compliance is not about defining terms. It is about understanding what kind of change you are investing in.

Generative AI improves compliance tasks. It makes a SAR narrative faster to draft, a case file faster to summarize, and a regulatory question faster to answer. These are real gains and institutions that have deployed generative AI well have seen measurable analyst productivity improvements. But generative AI is fundamentally reactive in that it responds to what you give it. Every step still requires a human to initiate, provide relevant context, and move the workflow forward.

Agentic AI changes compliance workflows. By giving it a goal rather than a prompt, an agentic system plans and executes the steps required to achieve it autonomously, using available tools and data sources, evaluating results, and adapting its approach along the way. One agent can manage hundreds more, and it continues to iterate until the goal is reached or it hits a decision point that requires human judgment.

It isn’t hard to understand how vast the practical implications of this are within compliance.

Given a suspicious transaction alert, AI agents autonomously retrieve the customer’s transaction history, check their profile against sanctions and PEP lists, search adverse media, map network relationships, and assess the alert against known typologies. A manager agent can then take all of this information and present it to the human investigator with a structured, evidence-based summary (all before the analyst has opened the case). The investigator’s role shifts from data gatherer to decision-maker.

That is not a faster version of the same workflow. It is a completely different operating model. It is why the Accenture Banking Top Trends 2026 report describes agentic AI as enabling the “10x bank”, where growth is no longer constrained by headcount, but by an organization’s ability to deploy and govern human-and-agent workflows at scale. For compliance specifically, the limiting factor is no longer analyst capacity, but the quality of the agentic infrastructure and governance around it.

Why compliance operations need agentic AI

The operational case for agentic AI in financial services compliance is clear from the responses in the FinCrime Frontier 2025-26 survey :

- More than 70% of financial institutions still rely on manual operations for at least half of their AML activities

- Alert fatigue affects 30.8% of institutions, which are identified as a primary driver of analyst inefficiency

- 65.6% of respondents cite poor data quality and integration as the single biggest drag on AML effectiveness

- 54% of compliance teams report that fewer than 5% of alerts lead to a case escalation or SAR filing, meaning most of an analyst’s time is consumed by work that produces no investigative output at all.

These numbers describe a compliance function under structural strain. The problem isn’t that analysts are working badly but that the operating model (alert-driven, manually intensive, and dependent on human data gathering before human judgment can be applied) is consuming capacity that should be reserved for the cases that actually matter.

Scaling this model through hiring is neither economically sustainable nor operationally effective. An organization cannot hire their way out of structural efficiency. Besides, the regulatory environment is moving in the opposite direction with regulators not asking for more activity, but for demonstrably better outcomes, which include higher-quality SARs, more accurate risk assessments, and faster detection of genuine threats.

Agentic AI addresses this at the structural level.

It doesn’t make analysts faster at the same work but removes the low-value work entirely, leaving them to apply their judgment where it genuinely matters.

What AI agents actually do: Four compliance workflow examples

Vague claims about AI transforming compliance are not useful to a CCO building a business case or a board seeking assurance. What is useful is precision about what AI agents actually do in specific workflows. With that in mind, here are four of the most significant.

Alert triage and pre-investigation

This is the highest-volume, highest-friction point in most compliance operations. An alert fires and someone has to assess whether it represents genuine risk.

In a conventional model, that means an analyst opening the case, pulling transaction data, checking the customer profile, running screening checks, and making a decision, which often takes 30 to 90 minutes per alert (for a queue that may contain thousands).

An agentic triage system runs this process autonomously for every alert, in parallel, before any analyst is involved. It evaluates the alert in full context taking into account customer history, peer behavior, product risk, channel signals, network relationships, and relevant typologies. Alerts assessed as low risk are automatically closed with documented reasoning written in an understandable manner for an auditor or regulator. The alerts that pose a genuine risk are escalated to analysts with the pre-investigation work already complete. Implementations of intelligent alert triage have delivered false positive reductions of 30-50% within months of deployment, releasing analyst capacity for higher value work.

Autonomous sanctions screening and entity resolution

Modern sanctions screening involves matching customer and counterparty names against frequently updated lists, resolving ambiguous matches, and making defensible decisions at scale.

Legacy name-matching generates large volumes of false alerts (variant spellings, common names, etc.) that consume investigator time on obvious non-matches. Agentic AI approaches entity resolution differently; rather than flagging every partial match and routing it to a human, an agent can autonomously gather additional identifying information, cross-reference multiple data sources, assess the probability that a match is genuine, and either close obvious false positives with documented reasoning or escalate genuine ambiguities for human review.

The result is autonomous sanctions screening that dramatically reduces the volume of false positive reviews without reducing the rigor of genuine match assessment.

AI-powered case management and SAR preparation

Within conventional compliance, case management is largely about assembling data. The investigator gathers information from multiple systems, constructs a narrative, identifies the relevant typology, and drafts the SAR. All of this takes time that could be better spent elsewhere.

Thankfully, agentic AI can handle the assembly and structuring autonomously. Agents can pull transaction data, adverse media, entity relationships, and typology references into a structured case file and generate a draft SAR narrative, which the investigator reviews, refines, and authorizes.

Reducing SAR drafting time by 40-60% is consistently achievable with well-implemented agentic case management, while the filing quality also improves because of the AI drawing on a wider, more consistently assembled evidence base than manual case preparation typically achieves.

Dynamic customer risk scoring

Traditional customer risk assessment produces a score when onboarding and refreshes it on a periodic schedule.

The agentic approach continuously re-evaluates risk as new information becomes available, such as:

- Adverse media hits

- Transaction behavior changes

- Network relationship changes

- Sanctions updates

- PEP designation events

The agent doesn’t wait for the 1-,3-, or 5-year review. It monitors continuously, re-scores dynamically, and triggers the appropriate response when a material change occurs. This is the operational engine of the Always-on Compliance™ model described in a companion article on perpetual KYC , and it represents a fundamental shift from periodic risk assessment to continuously maintained risk intelligence.

Multi-agent orchestration: When AI agents work together

Individual AI agents are great but the most significant gains in advanced agentic AI deployments are found with multi-agent orchestration, where multiple specialized agents collaborate on complex workflows, each contributing their specific capability to a shared goal.

In a financial crime investigation, this might work as follows:

- A detection agent identifies an anomalous transaction pattern

- An entity resolution agent autonomously researches the customer’s network relationships and beneficial ownership structure

- An adverse media agent scans open-source intelligence and regulatory publications for relevant negative mentions

- A typology matching agent assesses the pattern against known financial crime methodologies

- An orchestration layer coordinates the outputs of all four agents, assembles a coherent risk picture, and determines whether the evidence can be resolved independently or whether it requires human review.

This is what multi-agent AI financial crime investigation looks like in practice. The orchestration layer is the critical component, managing the sequencing, resolving conflicts between agent outputs, maintaining the audit trail, and ensuring that human judgment enters the process at the defined governance points.

The practical implication for compliance leaders is massive. This isn’t just about improving singular workflows, but completely changing the operating model to great effect with a multi-agent orchestration layer.

Governance and human-in-the-loop

Regulators are not opposed to AI in compliance. In fact, the FCA , FinCEN , FATF , and the new EU AMLA are broadly supportive of innovation within the sector. Even so, when it comes to agentic AI in regulated financial services, they are rightly asking tough questions about governance including wanting to understand what decisions does the AI make, what does it recommend, what guardrails are in place, what requires human sign-off, and how is every decision documented?

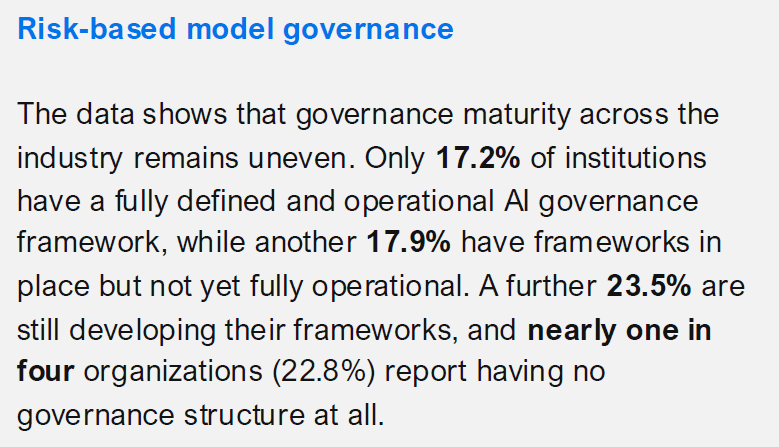

The FinCrime Frontier survey found that only 17.2% of financial institutions have a fully defined and operational AI governance framework, and 22.8% have no governance structure at all. This is the most significant differentiator between institutions that will successfully scale agentic AI and those that will face regulatory friction when they try.

The governance model for agentic AI in compliance is built on four principles:

Human-in-the-loop at defined decision points. Agentic AI should not be making important final decisions by itself. What it should be doing is handling the preparation, investigation, and structured reasoning (that currently consumes analyst time) and presenting a human with its recommendation for review. The survey found that 69% of institutions rely on human reviewers to validate alert relevance, which is the correct way of working, and makes the most of their expertise.

Explainability and auditability by design. Every decision an agentic system makes must be documented with sufficient context for supervisory review. Not just a score or a binary decision, but the reasoning. This means including what data was assessed, what pattern was identified, what typology was referenced, and why the system reached the conclusion it did. Explainable AI in AML compliance should not be seen as a feature but a regulatory requirement. After all, an agentic system that produces opaque outputs is a liability, not an asset.

Model governance and drift monitoring. AI models degrade over time as real-world patterns evolve beyond the data they were trained on. A compliance AI governance framework requires a named Model Risk Owner, regular validation against the Federal Reserve’s SR 11-7 guidance or equivalent standards, and mechanisms for detecting and correcting model drift before it affects detection quality. Alongside this, it is important to note that the EU AI Act adds a further layer of formal governance requirements for high-risk AI systems, with AI used in financial crime compliance almost certainly qualifying.

Escalation protocols. When an agentic system encounters a scenario outside its training distribution (an unusual typology, an ambiguous entity, a case with conflicting signals) it should escalate rather than decide. Defining these escalation protocols in advance and testing them regularly is a governance requirement.

Once your agentic AI governance is in place, what is it that regulators are saying?

Regulators and responsible AI in banking

Just like every other industry that is seeing the potential of AI, the regulatory landscape in financial services is developing rapidly, and compliance leaders need to understand its direction of travel.

Global

Globally, the FATF Recommendation 15 on new technologies requires financial institutions to assess and mitigate the risks associated with new technology, including AI. The guidance explicitly addresses the need for human oversight and the auditability of automated decision-making. Institutions that deploy agentic AI without documented governance frameworks are creating regulatory exposure.

Europe

The EU AI Act classifies AI systems used in financial services for credit scoring, fraud detection, and AML as high risk, imposing requirements for transparency, human oversight, technical documentation, and conformity assessment before deployment. While the Act’s implementation timeline is phased, institutions deploying agentic AI in compliance workflows should be building to these standards now, not retroactively.

In the UK, the approach of the FCA has been to encourage responsible AI innovation through its regulatory sandbox and innovation pathways while maintaining clear expectations about explainability and accountability. Put simply, the consistent message from the FCA is that the benefits of AI adoption are available to institutions that can demonstrate they understand and govern the technology.

US

In the United States, FinCEN’s modernization agenda and the banking agencies’ model risk management frameworks (SR 11-7) set the governance standards that apply to AI models in compliance. These frameworks predate the current wave of agentic AI but apply fully to it with any model that influences a material compliance decision requiring validation, documentation, and ongoing monitoring.

APAC

As explored in depth in a dedicated article on agentic AI regulation in APAC , there is currently no jurisdiction-specific regulatory guidance on agentic AI across Australia, Singapore, New Zealand, or Malaysia. In fact, New South Wales in Australia stands as the only APAC jurisdiction with dedicated agentic AI guidance, and that applies to the public sector rather than financial services. What regulators across the region do expect, however, is entirely consistent with their counterparts elsewhere - human accountability must remain central, model risk management frameworks must be extended explicitly to cover autonomous AI components, and explainability and transparency are non-negotiable.

The regulatory direction then, is consistent across all major jurisdictions with institutions that build governance infrastructure much better positioned to adopt agentic AI without regulatory friction.

How to implement AI agents in AML workflows: A practical roadmap

If moving from understanding agentic AI to implementing it, a practical roadmap reduces risk and builds the foundation that more advanced capabilities require. But where to begin?

Start with intelligent alert triage. This is the highest volume, most immediately measurable entry point. Deploying agentic triage models that evaluate alerts in full context before analysts are involved delivers false positive reductions of 30-50% within months, creates visible proof of value for the business case, and begins building the feedback data that trains next-generation detection models. Alert triage is also the lowest governance risk entry point because the agent is merely recommending, not making a final decision.

Establish governance infrastructure in parallel. Not doing this is the single most common mistake in agentic AI adoption in regulated environments because the problems will escalate down the road. With this in mind, appoint a named AI Model Risk Owner before the first agent goes into production. Define human-in-the-loop requirements for each workflow, establish the audit trail requirements, create escalation protocols, and build the model validation framework. Your future self will thank you because retrofitting governance after regulatory scrutiny arrives is both expensive and unreliable.

Expand to SAR narrative assistance and dynamic risk scoring. Once triage is delivering measurable value and governance is operational, the next layer is AI-assisted SAR preparation and event-driven customer risk scoring . These are more complex deployments and will have a greater productivity impact but can’t be done immediately. This is because they require the data quality and governance foundations that the triage phase establishes.

Move toward multi-agent orchestration. As individual agents earn trust and the governance framework matures, the capability sequence leads toward multi-agent workflows that automate end-to-end investigation processes. Investigations that previously took days are completed in hours, with analyst time focused entirely on decision-making.

The agentic AI compliance ROI case that emerges from this sequence is compelling. The FinCrime Frontier survey data and documented implementations support false positive reductions of 40-70%, SAR filing cycle time reductions of over 50%, and analyst productivity improvements of 30-60%, with ROI typically achieved within 8-18 months of initial deployment.

What agentic AI means for compliance analysts

One question that compliance leaders consistently raise is what agentic AI means for their teams. It is a legitimate question and deserves an honest answer rather than reassuring platitudes.

The honest answer is that agentic AI will change what compliance analysts do, but not by eliminating the need for human judgment in financial crime compliance. The complexity of financial crime (the contextual nuance, the jurisdictional variation, the evolving typologies, the judgment calls that sit at the boundary between suspicious and explainable) cannot be fully automated. Hopefully this article has made clear that what agentic AI does is to remove the mechanical, data-intensive, low-judgment work that currently consumes the majority of an analyst’s time.

As agentic AI use becomes more commonplace, compliance teams of the near future will spend:

- Less time gathering information and more time evaluating it

- Less time on obvious false positives and more time on genuinely ambiguous cases

- Less time drafting and more time reviewing and authorizing

The skills that will be most valuable in an AI-augmented compliance team are those that AI cannot replicate such as regulatory judgment, contextual reasoning, investigative intuition developed through experience, and the ability to engage critically with AI-generated outputs rather than accepting them with minimal oversight.

This upgrade of the analyst role requires deliberate investment in training and change management. Analysts who have spent their careers processing alert queues need support in developing the skills that will define their value in an AI-assisted environment. Institutions that invest in this transition will be able to enjoy productivity gains alongside retaining and developing experienced compliance talent.

Key takeaways for compliance leaders evaluating agentic AI in financial services

- For compliance, agentic AI is much more operationally significant than generative AI by a considerable margin.

- More than 70% of institutions rely on manual operations for at least half of their AML activities. Over half report that fewer than 5% of alerts lead to a SAR filing. Agentic AI addresses these inefficiencies at the structural level.

- Ask vendors to describe the specific workflow - what triggers an agent, what data sources it accesses, what guardrails are in place, what decisions it makes autonomously, where human review enters the process, and how every decision is documented. Vague claims about AI transformation are not sufficient.

- Human-in-the-loop is an important part of governance. The goal is not to replace human judgment but to ensure it is applied where it adds the most value. Regulators expect this model, and well-designed agentic systems are built around it.

- Only 17.2% of institutions have a fully operational AI governance framework. Building governance before deployment (not as an afterthought) makes agentic AI adoption in regulated environments both durable and scalable.

- The capability sequence matters. Start with alert triage, establish governance, expand to SAR assistance and dynamic risk scoring, and build toward multi-agent orchestration. Each step builds the foundation that the next requires.

- The regulatory direction is supportive with the FCA , FinCEN , FATF , and EU AMLA all broadly supportive of governed AI-driven compliance innovation.

- The ROI on agentic AI is impressive with false positive reductions of 40-70%, SAR cycle time reductions of 50%+, and analyst productivity improvements of 30-60% achievable within 8-18 months.

Related resources

Eliminating 90% of manual work in FinCrime compliance

Agentic AI, data, and financial crime control

Understanding agentic AI for financial crime prevention

The power of agentic AI for AML operations

Why regulators love agentic AI

Guide to Explainable AI in Financial Services

The future of financial crime prevention

SymphonyAI FinCrime Frontier 2025-26 Survey Report

Learn more about Symphony Risk Intelligence

Find out more about Symphony Risk Intelligence and Always-on Compliance, and how it can improve your approach to transaction monitoring, KYC/CDD, fraud, and screening.

Generative AI responds to prompts and produces content, making individual tasks faster but leaving the workflow itself unchanged. Agentic AI pursues goals autonomously across multiple steps, gathering data, making assessments, and completing workflows end-to-end without human prompting at each stage. For compliance specifically, that distinction separates a productivity tool from an operating model transformation.

An AI agent in AML compliance is given a defined goal (such as triaging an alert or investigating a sanctions match) and autonomously executes the steps required to complete it: retrieving transaction history, checking customer profiles, searching adverse media, assessing typology patterns, and producing a structured, evidence-based recommendation for human review. The agent draws on multiple data sources simultaneously and documents its reasoning at every step for regulatory auditability. Human investigators then apply their judgment to the agent's output rather than spending their time on data gathering.

Regulators across the US, UK, EU, and APAC are broadly supportive of AI-driven compliance innovation, including agentic AI, provided it is appropriately governed. The key requirements are consistent across jurisdictions: human oversight at defined decision points, explainable and auditable AI outputs, documented model governance, and clear escalation protocols for edge cases. Institutions that build governance infrastructure before deployment are better positioned with regulators than those that treat it as an afterthought.

Human-in-the-loop (HITL) is a governance principle requiring that human judgment is a mandatory input at defined points in any AI-driven compliance workflow. In practice, it means agentic AI handles data gathering, pattern assessment, and structured reasoning autonomously, while a qualified human reviews the output and makes the final consequential decision. The goal is not to slow down the process but to ensure accountability and auditability at the points where regulatory and reputational risk is highest.

Documented implementations support false positive reductions of 40-70%, SAR drafting cycle time reductions of over 50%, and analyst productivity improvements of 30-60%, with ROI typically achieved within 8-18 months of initial deployment. The strongest returns come from alert triage automation, which delivers measurable cost savings quickly while building the data foundation for more advanced capabilities. The SymphonyAI FinCrime Frontier 2025-26 survey found that only 28% of compliance professionals have formally measured their compliance technology ROI, making baseline measurement the essential first step before evaluating any agentic AI investment.

Henry Fosdike is Content Manager at SymphonyAI’s financial services division, bringing 10+ years of expertise in crafting compelling B2B, B2C, and D2C content to the world of AI-driven financial crime prevention technology. With a rich background, Henry excels at translating complex AI, finance, and SaaS concepts into clear, engaging narratives. His insightful articles and whitepapers demystify cutting-edge anti-financial crime solutions, providing readers with valuable knowledge and offering readers a deeper understanding of this rapidly evolving field.